- A new regulation framework will encourage the entrance of more digital banks with innovative offerings and services

- Diverse digital banking models are offered in the region with differentiated value proposition

- The region will offer more opportunities than challenges to digital banks

In recent years, customers expressed high demand for digital banking solutions. The pandemic further amplified the need for online services. Thus, neobanks emerged with new business models to challenge the traditional way of banking.

The United Arab Emirates (UAE), Saudi Arabia, Qatar, and Bahrain are among the key markets in the Middle East. According to the federal competitiveness and statistics authority in the UAE, 90% of its people use digital banking channels. They use internet banking for new products as well as mobile banking for transactions. In Saudi Arabia, digital banks mainly focus on individuals and small and medium-sized enterprises (SMEs) in the medium to long term. Young tech-savvy consumers who make up over 65% of its population are likewise primary target market of digital banks.

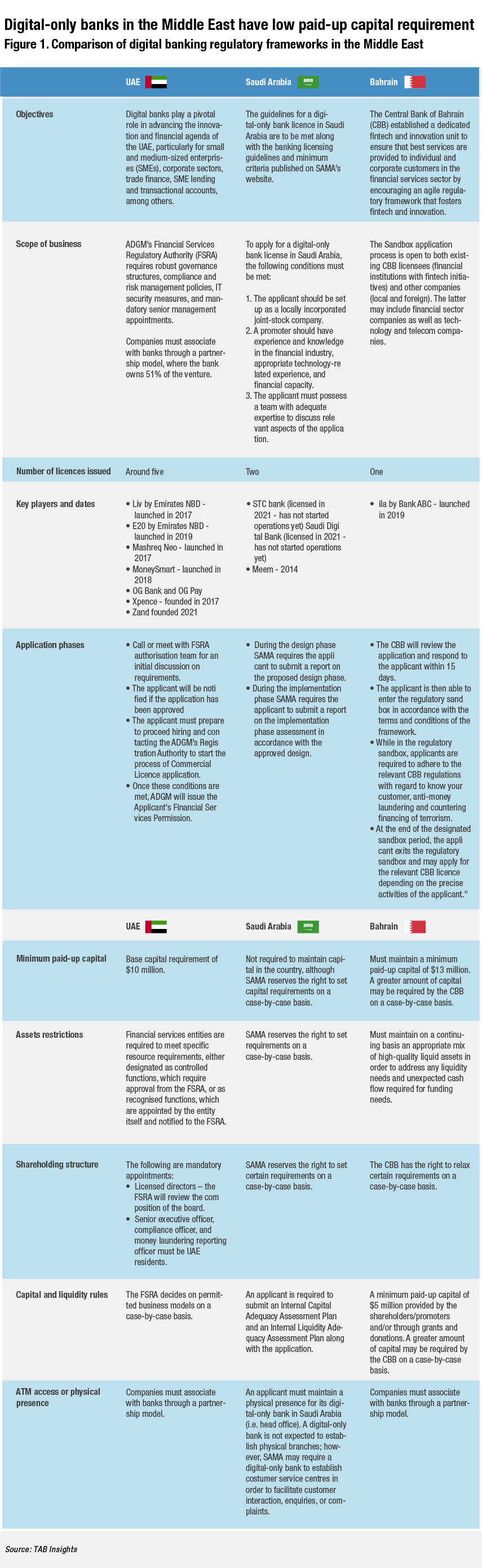

In the UAE, the Abu Dhabi Global Market (ADGM) launched in 2015 a regulatory framework for banks applying for a digital banking licence. It focuses on conventional banks seeking to establish digital banks or branches of digital banks, as well as for financial technology (fintech) companies with innovative value propositions. Application for a digital bank licence required a partnership between technology companies and financial institutions.

Saudi Arabia is leading the digital banking market. In June 2021, authorities granted two licences for digital-only bank STC Pay and a firm led by Abdul Rahman Bin Saad Al-Rashed and Sons Company. STC Pay will become a digital bank with a capital of SAR 2.5 billion ($666.7 million). The company will inject an additional $213 million (SAR 802 million) to retain 85% of its share capital. Meanwhile, Abdul Rahman Bin Saad Al-Rashed and Sons Company will lead a local digital bank to conduct banking business in the country with a capital of SAR 1.5 billion ($400 million).

In February 2020, the Saudi Arabian Monetary Authority (SAMA) introduced licensing guidelines for digital-only banks. The guidelines set out the minimum requirements that applicants must meet in order to obtain a digital-only bank licence. This milestone initiative aims to align with the objectives of the Financial Sector Development Programme (FSDP) and Saudi Vision 2030 by developing the digital economy.

SAMA also implemented a supervision framework to include aspects of technology, cybersecurity, anti-money laundering, tracking terrorist financing as well as operational risks.

Digital banking landscape is expanding in the Middle East

In recent years, the market has seen a variety of digital platforms with a wide range of financial services presented to customers. This led to the creation of neobanks. Compared with traditional banking, neobanks can offer diverse services at lower cost. As customers became more open to use digital services, they required more flexibility and ease of use. In the Middle East, authorities are exerting efforts to develop the digital banking sector and encourage innovation. Saudi Arabia and the UAE are taking the lead in this space in the region. There is a high potential for further growth, especially with changes to consumer behaviour and new regulations for digital-only banks.

The Middle East has diverse digital banking models

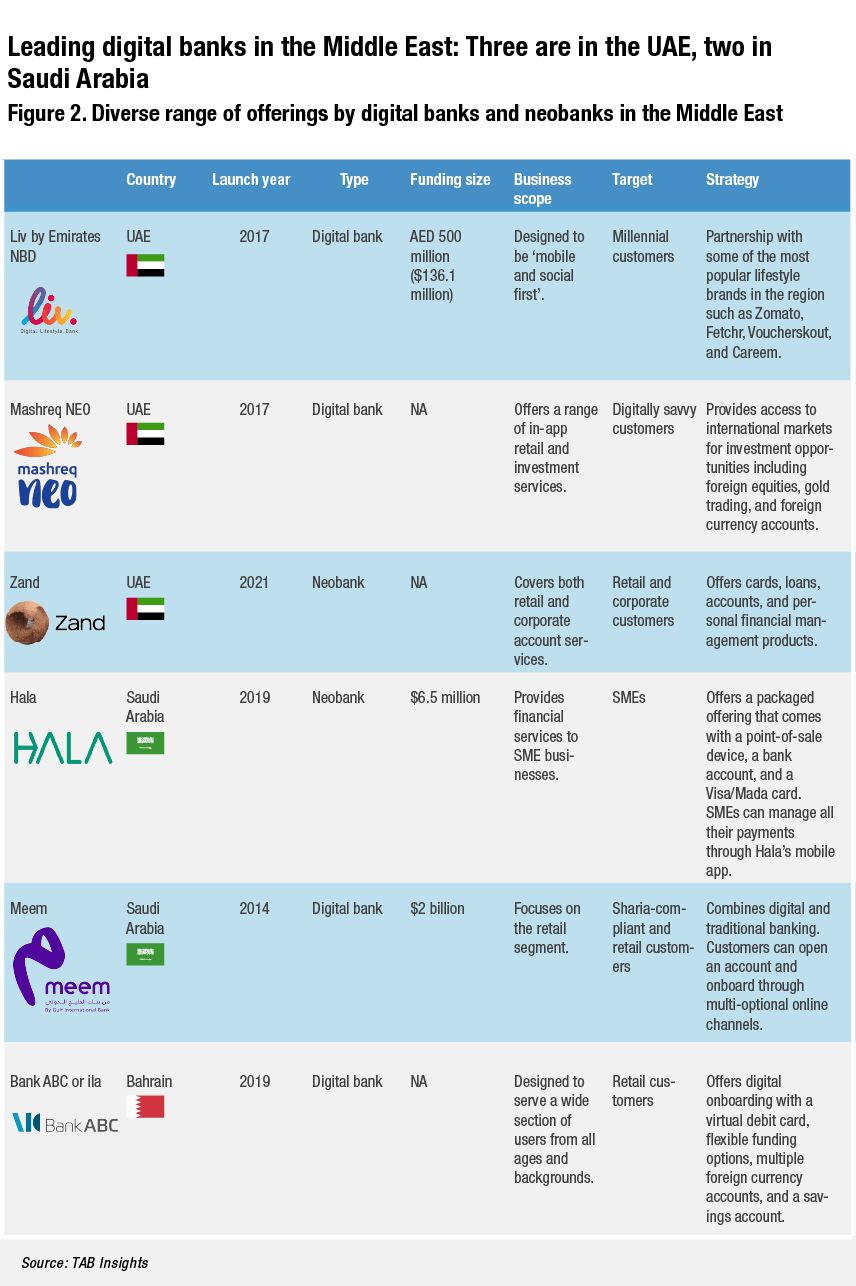

Liv by Emirates NBD and Mashreq Neo in the UAE are among the front-end digital banks backed by large traditional banking or non-bank institutions. Mashreq Neo was launched by Mashreq Bank in 2017. It is completely branchless and targets the digitally savvy generation. Liv by Emirates NBD was also launched in 2017 as a digital lifestyle bank to attract millennials. It has onboarded more than 300,000 clients since its inception. In Saudi Arabia, Gulf International Bank introduced Meem, a sharia-compliant digital bank that offers banking services to Bahraini and Saudi customers. In Bahrain, Bank ABC introduced its digital bank ila in 2019 with the goal to expand in the Middle East and North Africa region.

Stand-alone neobanks are 100% digital and have no physical branches. They mainly operate through a mobile application or online platforms. It is the primary contact point of customers. Neobanks use data to understand the behaviour of customers and create few offers that match their needs. As a result, customers have access to innovative offers with excellent services and a personalised experience. Hala Bank has acquired digital banking licences from SAMA and the ADGM’s FSRA in Saudi Arabia and the UAE respectively. The UAE granted a banking licence to Zand to become a fully independent digital bank in the country. With the licence, Zand will be able to provide innovative solutions that address the needs of retail and corporate customers.

Opportunities and challenges

Neobanking is still in the nascent stage in the region, as the market is still dominated by the traditional banking model that has physical branches. The conservative model of the financial sector, reluctance to change and the absence of adequate regulatory framework impede the growth of neobanking.

Absence of adequate regulatory frameworks a barrier

For instance, the regulatory framework in the UAE requires fintech companies to partner with a banking institution before it is granted a digital banking licence. In order for neobanks to legally operate, they have to partner with a traditional bank and use their licence with a revenue-sharing agreement in return. Thus, the complex regulations and cultural differences pose challenges to banks wanting to enter the UAE’s fintech space. These barriers make it difficult for digital-only banks to emerge.

Traditional banks are adapting their digital strategy

Existing regulatory frameworks tend to favour traditional banks. However, the widespread penetration of internet and smartphones forced these banks to reassess their digital strategy. Thus, they built digital infrastructure and diversified their offerings through online channels and apps. At the same time, the emergence of fintech startups has disrupted the financial services industry by demonstrating a technological innovation capability with new personalised services to cater to the changing consumer demands. As a result, banks have introduced new digital offerings such as Liv by Emirates NBD, Meem by Gulf International Bank, and Mashreq Neo by Mashreq Bank.

There is a significant opportunity in the region in the digital banking landscape. According to the UAE government portal, there are around 18.3 million mobile phone users in the UAE. Traditional banks are also increasingly investing in technology as a way to stay competitive and address young consumers’ needs.

Market remains attractive to fintech companies

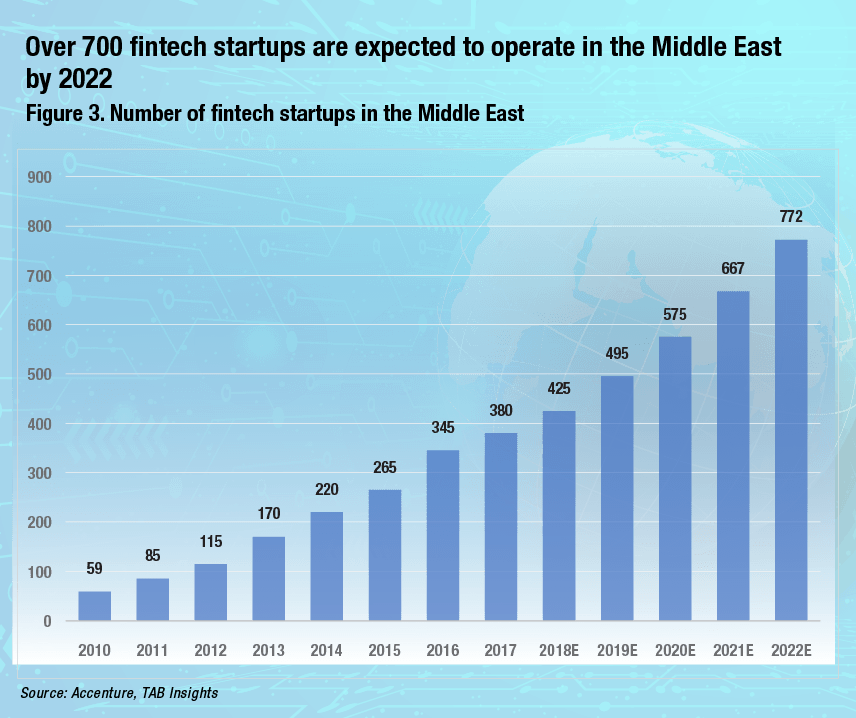

According to Finextra, the Middle East has attracted only about 1% of global fintech financing in 2018. However, this share is growing. Finextra projects that by 2022, around 465 fintech companies in the Middle East will raise over $2 billion in venture capital funding, compared with the 30 fintechs that raised nearly $80 million in 2017.

COVID-19 lockdowns accelerating the digital transformation

The series of lockdowns and health protocols enforced by governments amid the COVID-19 pandemic has enhanced consumers’ readiness to use digital financial services. Customer behaviour has significantly shifted to demand a contactless experience. This has led banks to accelerate their digital transformation and collaborate with fintech companies to build digital platforms and ensure better digital experience for customers while addressing cybersecurity risks.

The banking landscape in the Middle East will continue to witness traditional financial institutions revamping their strategies to stay relevant and adapt with the fast pace of change in customer behaviours. In addition, governments will shift their priorities to accelerate and regulate the digital space to align with their efforts on developing digital economies as one of their priorities. This will encourage more investment in the digital space. We expect to see more partnerships between banks and fintech companies, and digital bank will continue to work along with traditional banks to leverage from their customer base and presence in the market.

.png)

.webp)