Research Notes Aug 04

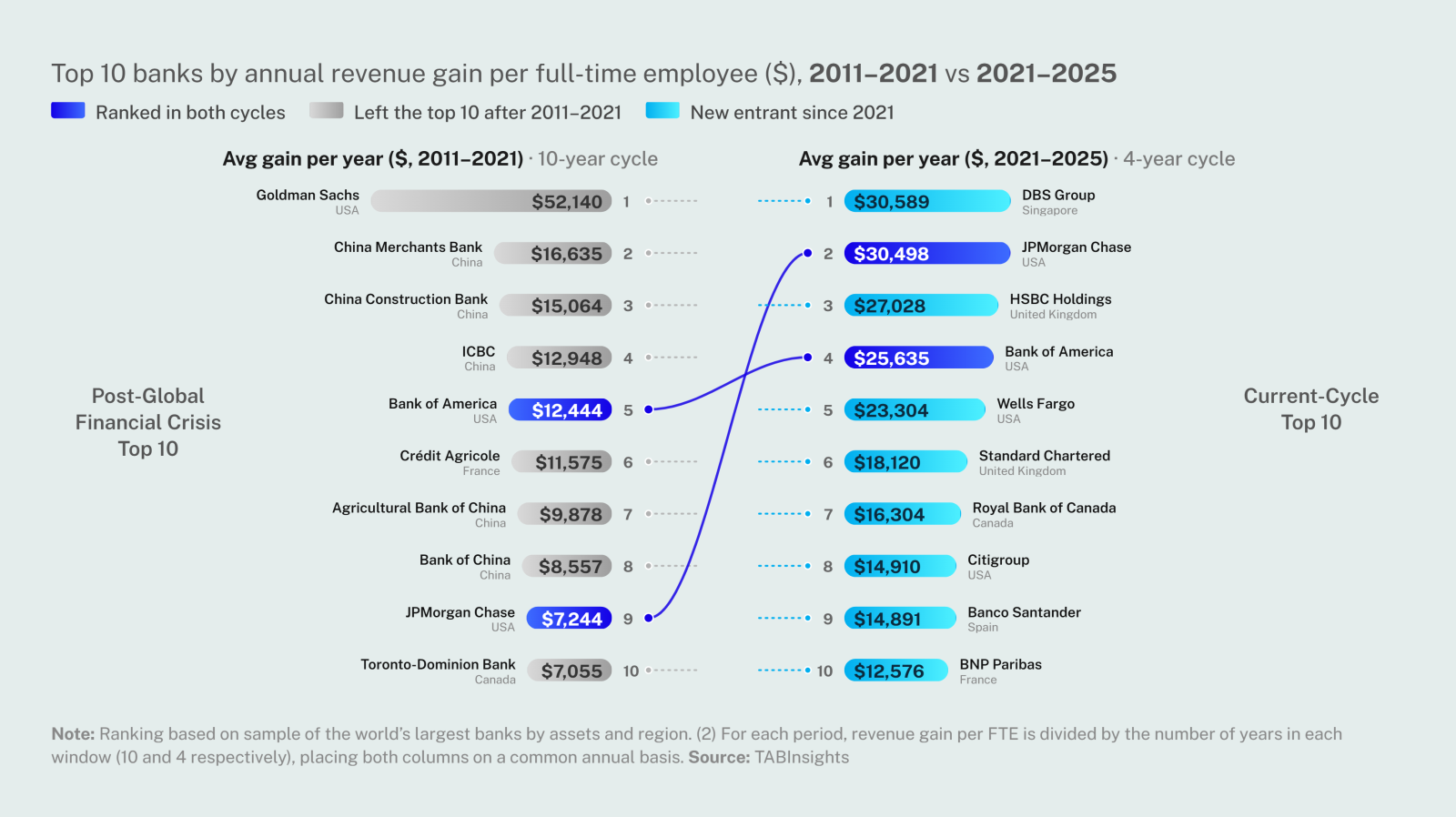

Data from 25 of the world’s largest banks by assets across regions shows that leading institutions are not only accelerating existing work but also building the capacity to serve more customers, process higher volumes of activity and grow revenue without increasing resources at the same pace.