China’s major banks have made notable progress in overseas expansion. Headline figures suggest growth, but closer analysis reveals structural limitations. Expansion has largely followed Chinese corporates abroad, supported by cross-border renminbi flows, rather than stemming from independently generated revenue. Scale has been achieved, but diversification remains limited.

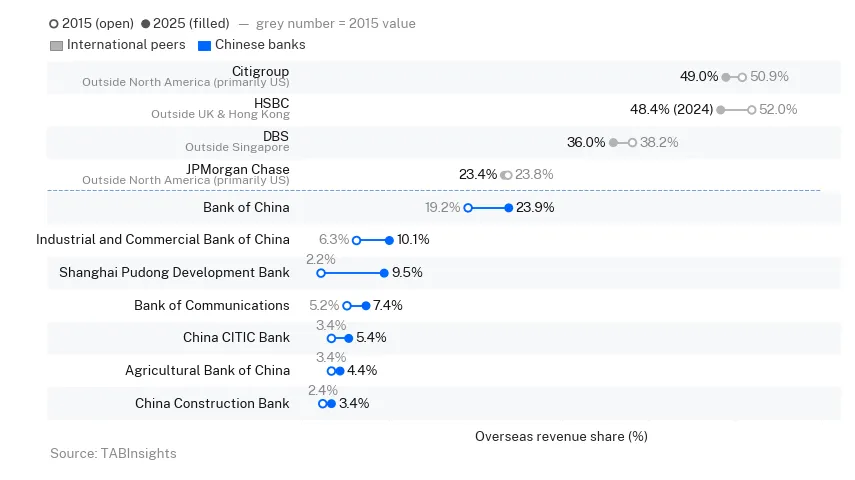

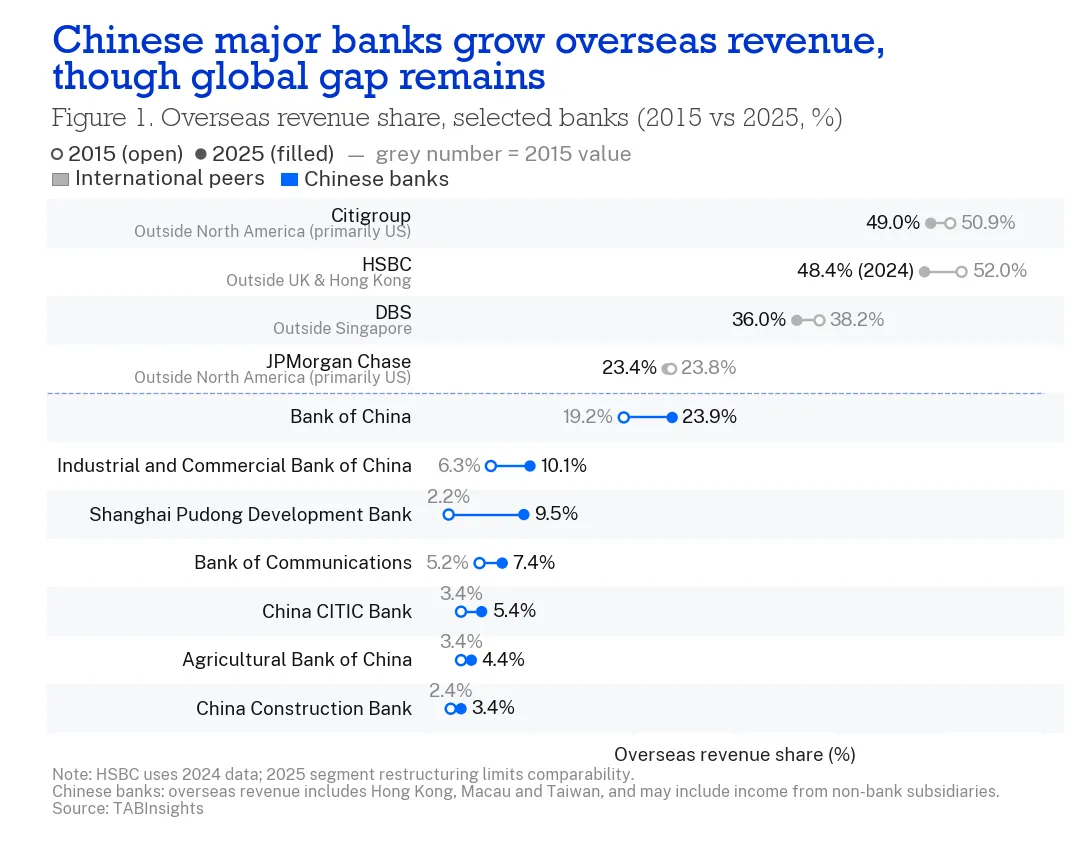

Bank of China (BOC) reported 23.9% of group revenue from overseas in 2025, the highest among domestic peers and superficially close to JPMorgan Chase's 23.4%. The composition tells a different story: around 80% of BOC's overseas revenue comes from Hong Kong, Macao and Taiwan, while revenue from the rest of the world represents only 4.8% of total group revenue. By contrast, JPMorgan's international revenue spans Europe, the Middle East, Africa, Asia Pacific and Latin America, anchored in wholesale banking, capital markets and corporate lending.

BOC's strength lies in its infrastructure reach rather than independent revenue generation. Its network covers 64 countries and regions, operates renminbi clearing in 18 markets, connects 46 direct and more than 780 indirect Cross-Border Interbank Payment System participants as of early 2026, and carries cumulative Belt and Road credit exposure of $439 billion by end-2025. These capabilities support Chinese corporate globalisation, yet converting them into proportional revenue remains challenging. Belt and Road facilities — long-tenor and infrastructure-linked — produce modest recurring income relative to capital committed.

Industrial and Commercial Bank of China (ICBC) has followed a steady trajectory, raising overseas revenue from 6.3% in 2015 to 10.1% in 2025 across 410 institutions in 49 countries. It serves as a clearing bank in 12 overseas markets, processes over RMB 10 trillion ($1.4 trillion) in cross-border renminbi business annually, and holds a 20% stake in Standard Bank Group, extending indirect reach across 21 African economies. ICBC frames international operations as a long-term growth frontier rather than as a supplementary business line.

Other major state banks remain more constrained. China Construction Bank reached 3.6% of overseas revenue in 2025 despite 22% year-on-year growth, and Agricultural Bank of China 4.5%, both prioritising integrated domestic–international services over aggressive geographic expansion, with overseas operations largely serving as coordination layers for outbound corporates. For some banks including ICBC, reported overseas revenue includes non-bank domestic subsidiaries, slightly inflating the comparability of figures.

Joint-stock banks paint a mixed picture. Shanghai Pudong Development Bank's overseas revenue rose from 2.2% in 2015 to 9.5% in 2025, despite volatility. The 2024 decline reflected higher credit provisions and reduced cross-border activity in emerging markets, while the 2025 rebound was partly driven by renewed renminbi lending in Southeast Asia. Bank of Communications reached 7.4% and China CITIC Bank 5.4%, reflecting steady internationalisation aligned with domestic client bases. China Everbright Bank and China Minsheng Bank fell back in 2025, exposing the fragility of thin franchises concentrated in few markets and lacking sufficient network depth.

The gap with global peers remains stark. HSBC generated 48.4% of revenue outside its core UK and Hong Kong markets in 2024, Citigroup 49% outside North America in 2025, and DBS 36% outside Singapore in 2025. Domestic opportunities in China offer substantial credit volumes and attractive returns, though net interest margin compression reinforces the need for international diversification. Belt and Road lending expanded balance sheets but generated limited recurring revenue, while renminbi internationalisation has largely tracked mainland corporates rather than building independent foreign client relationships.

The mode of internationalisation has shifted. Chinese banks have moved from branch-driven expansion to network optimisation and service densification, focusing on integrated platforms, centralised coordination and comprehensive product service chains. This approach mitigates the capital and regulatory costs of physical branches but suggests that international revenue share is unlikely to rise rapidly through network expansion alone.

BOC and ICBC remain the most internationalised Chinese banks, while others advance unevenly from lower bases. The key question is whether Chinese banks can establish self-sustaining revenue streams in foreign markets, moving beyond serving outbound mainland clients as renminbi internationalisation and corporate globalisation create new opportunities. Closing the gap with global peers will require converting infrastructure and currency advantages into global franchises, offering comprehensive products, building local market credibility, and competing on international terms.

.png)

.webp)