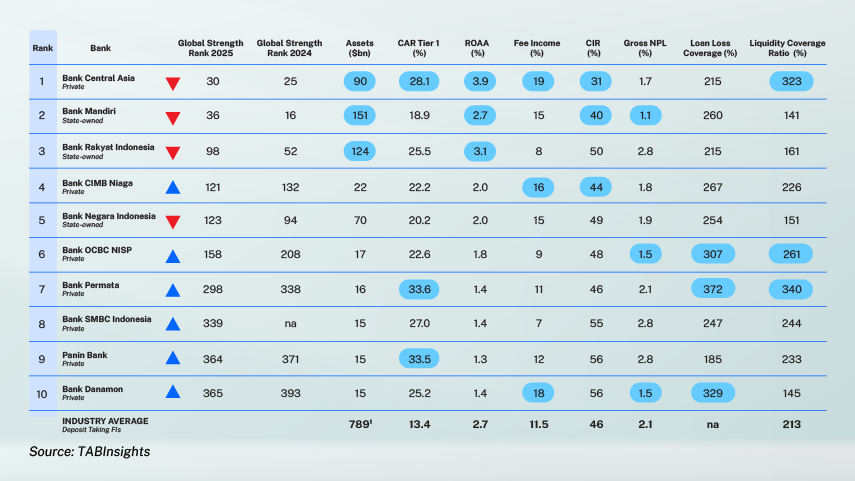

Among the 16 Indonesian commercial banks in the World’s 1000 Strongest Banks, Bank Central Asia (BCA) and Bank Mandiri emerged as Indonesia's leading banks, with BCA rising to the top spot in 2025, surpassing Mandiri, which held the position the year before.

BCA is ranked 30th globally, with Mandiri not far behind at 36th. Both banks surpass leading Southeast Asian competitors such as Maybank in Malaysia (69) and Kasikornbank in Thailand (106). They are also on par in overall strength with global institutions like Bank of America and the Commonwealth Bank of Australia.

The leading banks among the top 10 strongest banks in Indonesia are dominated by the four largest—BCA, Mandiri, BRI and BNI. However, all four of the largest banks dropped in the 2025 rankings. Indonesia's four largest banks faced a common set of headwinds in 2024: NIM compression as elevated Bank Indonesia rates raised funding costs, operating expense growth that outpaced revenue and loan books expanding significantly faster than deposit bases — pushing loan to deposit ratios sharply higher and tightening liquidity buffers.

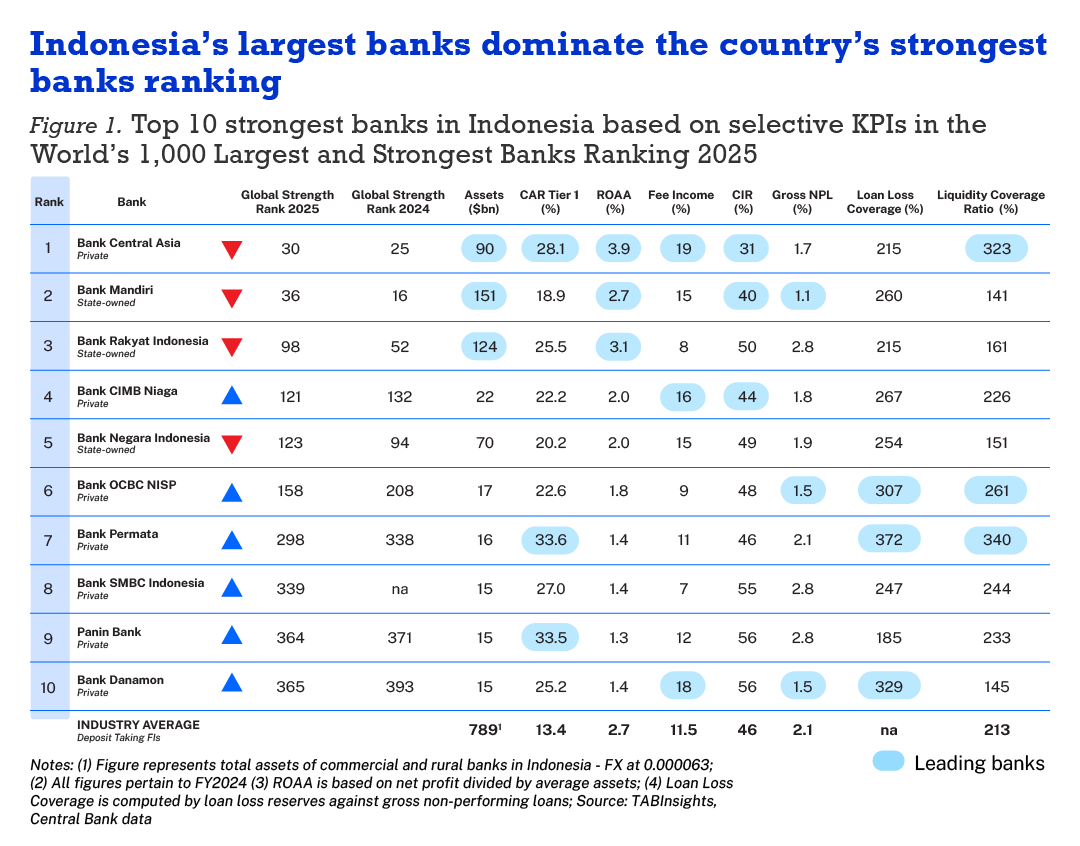

BCA was the exception: its CASA-dominant retail franchise insulating NIM and enabling superior cost discipline. The lender’s resilience through shifting credit and interest rate cycles is anchored in its consistently strong operating fundamentals, which has established it as a standout performer. This was supported by a larger retail portfolio (23% of total loans) compared to Bank Mandiri (17%).

Annual loan yield in Indonesia’s retail banking segment is in the range of 8-9%, versus 6-7% in corporate and commercial banking. BCA's model prioritises operational efficiency, enabling the lender to maintain high returns on assets, even in a highly competitive environment, while expanding its wholesale and digital banking services to complement its core retail strength. This disciplined approach to growth allowed BCA to outperform its peers, even amid broader market pressures. While the banking sector faced another challenging year in 2025, with the big four seeing a 4% decline in net profit, BCA stood out, achieving a 4.9% year-on-year growth in 2025.

In the current climate, banks have been pivoting towards corporate and commercial lending. Corporate loans led industry growth in 2025, while consumer loan growth remained flat. Indonesian industry loans saw a 10.3% CAGR from 2022 to 2024 as the economy recovered from the Covid-19 pandemic. In 2025, coming off a high-interest rate environment in 2024, loan growth in 2025 was less robust, with industry loans growing 9.7% year-on-year. Loans at BCA and Mandiri increased by 7.7% and 13.4%, respectively. Bank Indonesia reduced its benchmark interest rate five times starting in September 2024, from 6.00% to 4.75% by end-2025.

The industry has seen a rise in non-performing loans in consumer and working capital loans in 2025, with consumption loans rising fastest from 1.9% in 2024 to 2.4% as of October 2025, according to Otoritas Jasa Keuangan (OJK), Indonesia's financial services regulator. Banks expect the cost of credit to rise further in 2026. Credit risk could become more pronounced if economic growth further slows or corporate cash flows are squeezed from the impact of the Middle East crisis. Bank Indonesia projected GDP growth in its February meeting of about 4.9% to 5.7% in 2026 based on macroeconomic conditions before the crisis was factored in. Recent projections by the World Bank suggest that if the Strait of Hormuz remains restricted through most of 2026, growth could fall to 4.7%.

Against market and geopolitical headwinds, the top 10 strongest Indonesian banks remain well capitalised. Bank Permata’s Tier 1 capital ratio stands at 33.6%, Panin Bank at 33.5%, and BCA at 28.1%. All of these figures significantly exceed the OJK minimum requirement of 6%, as well as the average Tier 1 ratio of 14.9% among the 460 strongest banks in the Asia Pacific region. Indonesia's liquidity ratios are high by global standards too. Bank Permata posted a 340% liquidity coverage ratio (LCR) — among the highest in the entire dataset, BCA (323%), and Bank OCBC NISP (261%) all reflect very high liquidity buffers, likely driven by a structurally deposit-heavy funding mix and conservative asset allocation.

Together, those 10 banks held $550.1 billion in assets, 69% of total banking assets, generating $14.1 billion in net profit— with a return on average assets (ROAA) of 1.9% placing them above the global median of 0.9%. Average industry margins in Indonesia are among the highest in Asia Pacific with net interest margins of approximately 4.5%–5.0% in 2025.

Mandiri and BCA offer distinct strategies on path to profitability

Mandiri and BCA, while overlapping in commercial lending, transaction banking, retail and wealth management, are, at their core, competing for slightly different customer segments.

Mandiri is Indonesia's largest bank by assets, and that size advantage flows directly from its role as the primary financial partner of the Indonesian government, state-owned enterprises, and national infrastructure. In 2025, corporate and commercial lending grew by 23% and 12% year-on-year, respectively — doubling BCA's growth in corporate lending. As with BCA, consumer lending was flat at 1.4%. Corporate and commercial loans now make up 58% of Mandiri’s portfolio.

TAB Global named Mandiri the Best Corporate, Investment and Wholesale Bank in Indonesia in its 2025 ranking, supported by cross-border capabilities across seven countries that no domestic private bank replicates at equivalent scale.

BCA’s overall loan portfolio growth was driven more by sharia financing (23.1%) than corporate loans (11.5%) and commercial loans (8.5%) in 2025. Consumer loan growth was flat at 0.2%. Corporate and commercial loans contributed 64% to total loan book.

A key factor in BCA’s success is its strong growth in customer savings accounts (CASA), which increased by 13% year-on-year in 2025, contributing to a solid funding base. While Mandiri operates a substantially larger balance sheet, BCA generates structurally cheaper funding: above 85% from retail CASA deposits, which insulated its NIM from the five Bank Indonesia rate cuts in 2025 that compressed margins across the sector. Mandiri's CASA ratio of 68% — healthy but lower — reflects the cost of funding a wholesale-dominated book that requires more institutional and time deposit funding alongside its retail base.

BCA leads in profitability

The profitability gap in 2025 based on assets is significant. BCA's ROAA of 3.8% in 2025, against Mandiri's 2.4% in 2025, and CIR of 31%, the lowest of any major Indonesian bank, against Mandiri's 44%. BCA’s non-risk adjusted NIM of 5.7% is the highest in Indonesia's banking sector.

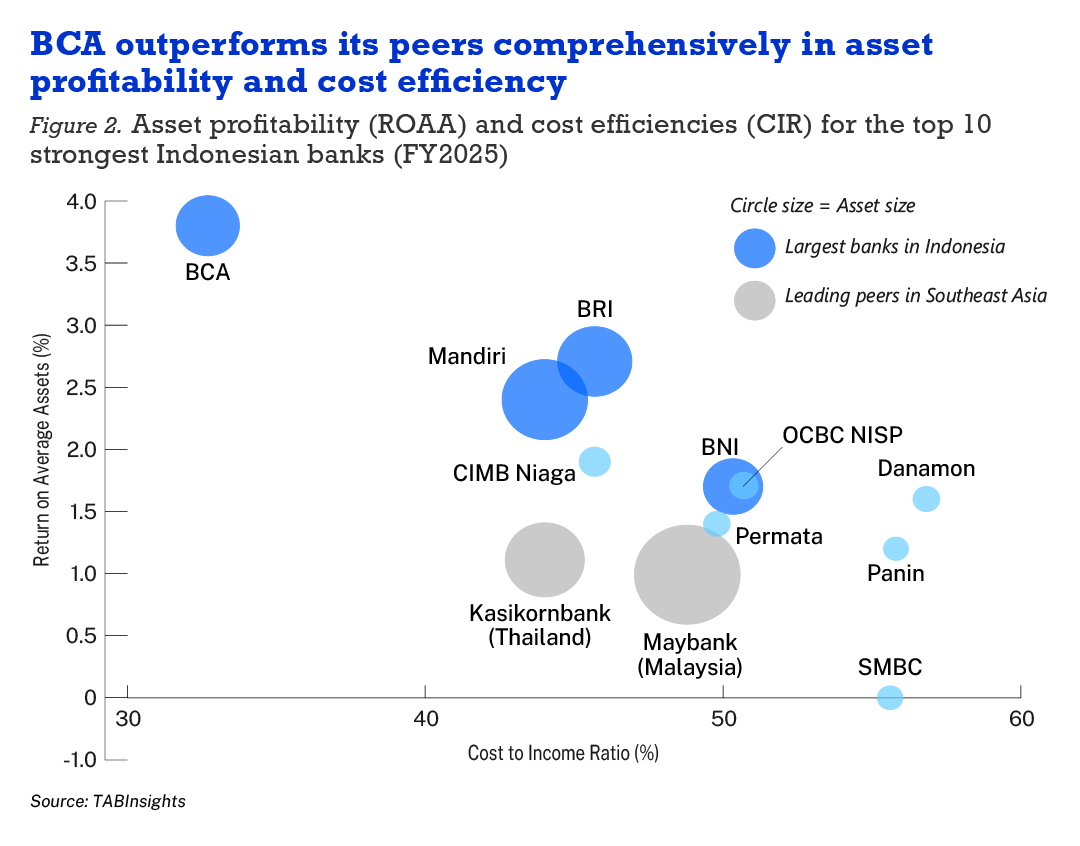

Yet on absolute net profit in 2025, the two banks are near-equivalent. Mandiri reported IDR 56.3 trillion ($3.5 billion) in net profit against BCA's IDR 57.5 trillion ($3.6 billion), despite Mandiri operating at 1.7 times the asset base. While this is driven by BCA's better capital and asset productivity, it also reflects Mandiri's structural challenge: generating adequate returns from large, lower-margin wholesale loans requires sustained volume growth that adds concentration risk, whereas BCA's retail model generates high-quality returns from a more diversified, sticky deposit base.

For the first time since 2022, BCA surpassed BRI and Mandiri to become the most profitable bank in absolute terms in 2025.

Mandiri has steadily improved asset quality since 2020

Mandiri holds the strongest asset quality position among the top 10 Indonesian banks, with a gross NPL ratio of 1.1% in 2024 and 0.96% in 2025 against industry NPL ratio of 2.2%. It significantly improved this ratio, reducing it from 3.1% in 2020. This was achieved through a proactive, data-driven strategy, leveraging digital Early Warning Systems and modern digital platforms like Kopra for corporate banking and Livin' for consumer banking. The improvement was further supported by strong credit restructuring and wholesale-led ecosystem lending.

The shift in leadership in profitability and asset quality between BCA and Bank Mandiri reflects portfolio structure rather than underwriting weakness: Mandiri's book is dominated by investment-grade SOE and corporate exposures that carry inherently lower default risk; BCA's book includes more retail and consumer lending. In a rising credit risk environment in 2025, both institutions maintained robust provisioning — Mandiri's loan loss reserves against non-performing loans stood at 260% in 2024 and 224% in 2025 and BCA held IDR 4.3 trillion ($250 million) in total provisioning in 2025.

Larger banks, including state-owned banks, outperform smaller peers in Indonesia

Competition among the largest banks has intensified, with improvements in funding and transaction capabilities narrowing existing gaps, including those involving state-owned banks. Unlike in India, where state-owned banks lag their private counterparts, Indonesian state-owned banks have built a strong, competitive corporate management layer over the past decade, now competing on equal footing with private banks.

However, this competitive shift has largely been driven by consolidation at the top, with larger banks capturing market share from smaller rivals. Market share by assets for the four largest banks in Indonesia rose from 54.8% in 2020 to 55.3% in 2024, according to data from Bank Indonesia, the country’s central bank. During the same period, the gap in operating income growth was even more pronounced relative to their 12 peers in the World’s 1000 Largest and Strongest Banks Ranking by operating income. The big four, despite their size, saw a 144% growth in operating income from 2020 to 2024, while the other 12 grew by just 119%.

For further insights on BCA, read the interview with Hendra Lembong, President Director of BCA.

View the complete World’s 1000 Largest and Strongest Banks Rankings.

.png)

.webp)