- SWIFT’s dominance is coming under threat from agile competitors and payments aggregators, but maintains it isn’t going anywhere

- Blockchain illustrates how systems such as self-sovereign identities mean that there’s more than just FX at play when it comes to payments

- Big banks are fighting back to take on regional fintech platforms and smaller banks will have to focus on domestic markets

Seamless digital transactions are already making banking less visible and more accessible, no matter who you are or where you live. To this end, cross-border payments are becoming a touchstone for financial innovation — and those who are not already thinking outside the box will be left behind.

We are seeing a rapidly evolving payment space. Features such as payments-as-a-service, one-click payments, invisible payments, spread payments and even payments subscription services all vie for market share in a landscape that has in recent years evolved away from traditional financial institutions (FIs) as the sole providers of these services. The adoption of ISO 20022, which facilitates transactions across borders between FIs and non-FIs, is increasing rapidly, with over 200 global initiatives already using the standard.

The coronavirus pandemic has also accelerated the move to cashless transactions globally, following a directive from the World Health Organization to use contactless payment wherever possible. At the height of the pandemic, some countries reported reductions in ATM withdrawals of 50% over just a few days. At the same time, the global payments economy has been significantly affected, with an estimated 25% to 30% decrease in cross-border consumer to business payments. However, the industry remains confident that the post-pandemic world will still see the cross-border payments sphere continuing its rapid evolution.

SWIFT says that old dogs can learn new tricks

In addition to moving into mid-market gaps left by traditional banks, agile payments aggregators such as Earthport and INTL FCStone have ushered in a new era of efficiency, speed and costs. In their attempts to “minimise SWIFT burdens,” they have exposed the transactions giant like never before.

Wim Raymaekers,

Global head of banking markets,

SWIFT

Chintan Shah,

Head of cash management in Asia Pacific,

Deutsche Bank

Wim Raymaekers, global head of banking markets at SWIFT, said that the global payments initiative (SWIFT gpi) shows that the Society hasn’t been left behind — pointedly noting that it believes in “responsible innovation.”

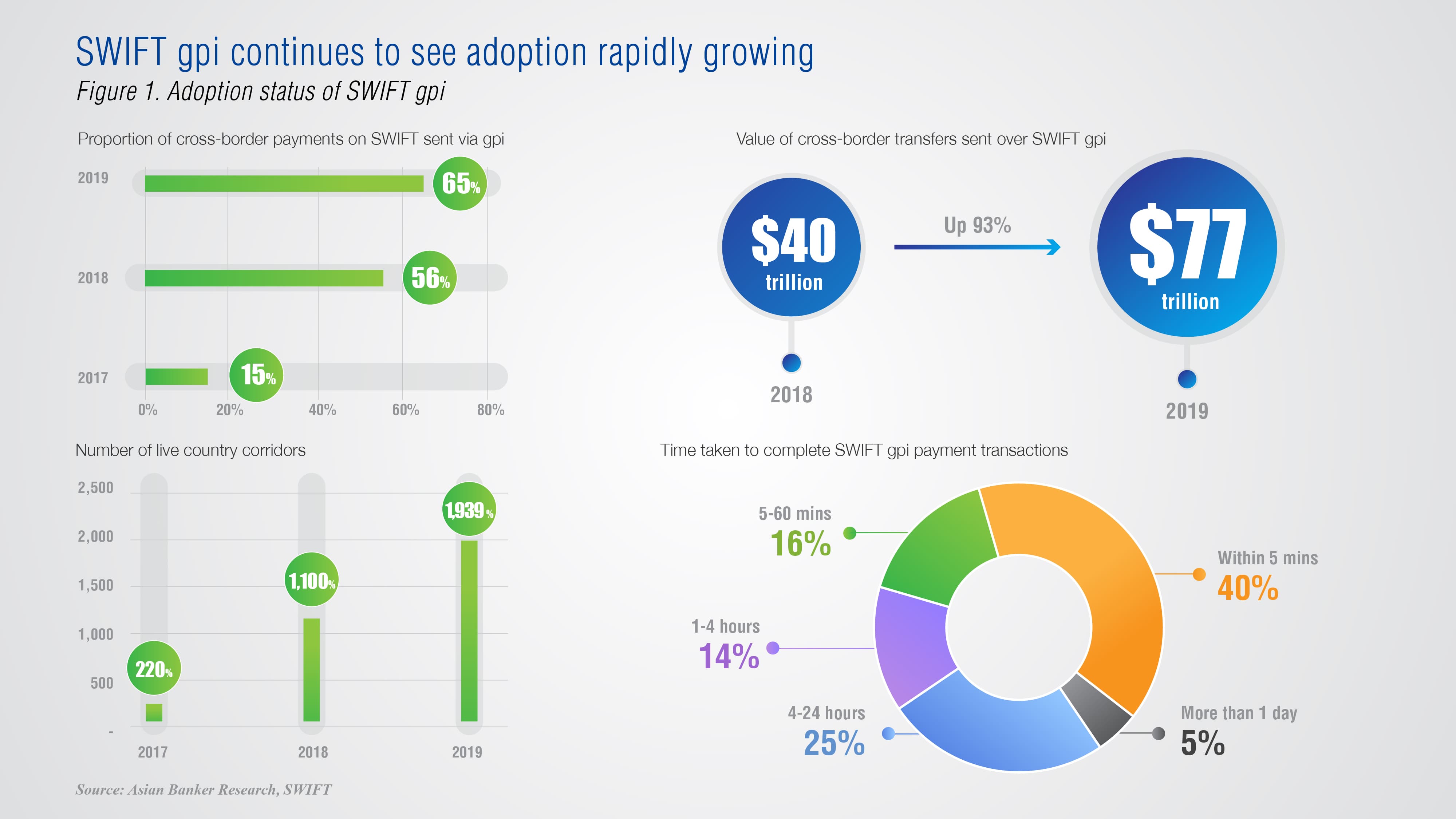

“Just three years since its launch, SWIFT gpi has been widely embraced by the community. In 2019, 65% of cross-border and intergroup payments were sent using gpi. That represented nearly $77 trillion in value, almost double the $40 trillion that moved through the service in 2018,” he added.

Raymaekers also said that SWIFT gpi has increased speed, with more than 50% of payments credited to end beneficiaries within 30 minutes. Speed is one important benefit of the new system, but so are the increased transparency and predictability of cross-border payment flows that gpi enables as well.

The September 2019 launch of gpi Instant can be seen as a sign of SWIFT feeling the heat from many of the new regional platforms that have emerged, particularly in Asia, for the $689-billion global remittances market.

“It integrates gpi into domestic instant payments systems around the world,” said Raymaekers. “This will facilitate instant international payments with up-front fee and foreign exchange transparency for senders, while also ensuring ubiquitous availability of instant cross-border payments globally.”

The initiative, which links domestic real-time networks such as PromptPay in Thailand, JomPay in Malaysia and FAST in Singapore to effect instant cross-border payment, is an attempt to entrench SWIFT as the dominant player in cross-border payments. In recent years, agile challengers to banks have emerged in the regional remittance space, with competitors coming from numerous angles including payment aggregation, blockchain, money transfer, and new FX players, such as mobile wallet and currency converter YouTrip.

In spite of Instant’s rapid transfers, banks will need to stay on their toes as new competitors are offering consumer-friendly product suites on top of near-instant global transfers. But for now, SWIFT and its client banks are touting the speed with the reliability of traditional banks.

Raymaekers noted that the launch followed a number of trials, including one which integrated SWIFT gpi Instant into Singapore’s domestic instant payment service FAST.

“It involved 17 banks across seven countries and saw payments between all continents settle within 25 seconds; the fastest in just 13 seconds. Successful trials have also taken place in Australia with the New Payments Platform and Europe with the European Central Bank.”

In April, Singapore’s NCS signed a memorandum of understanding with the Network for Electronic Transfers (NETS) Group to develop a new real-time electronic payment and securities settlement platform for central banks in the Asia Pacific region.

Whether through SWIFT’s enhanced capabilities or the new NCS-NETS platform, the linking up of individual real-time payment systems in Asia is a step towards catching up to SEPA — Single Euro Payments Area — and its enabling regulation PSD2. The PSD2 scheme, which came into effect in the European Union in September 2019, aims to reduce fraud by mandating multi-factor authentication for non-recurring online payment transactions over $32.59 (EUR 30). By potentially moving fraud away from Europe, it is predicted to have a ripple effect on the payments processing industry in Asia, the United States, and beyond.

Acceleration of digital favours bigger regional players

Chintan Shah, head of cash management in Asia Pacific for Deutsche Bank (DB), said that “clients are very keen to digitise their transaction flows” because of the COVID-19 crisis. He believes that FX conversion is the critical space, with DB rolling out an FX execution platform through SWIFT gpi, which allows clients to hedge FX exposure within an end-to-end, real-time and instant settlement experience.“Cross-border payments are a traditional business, so the measure is more on winning new clients. SWIFT gpi has made cross-border payments more efficient. In most markets, instant payments are a new payment scheme and we see most clients, especially in the B2C segment, adopt this aggressively,” Shah said.

He added that over 60% of Deutsche Bank’s cross-border payments are now settled in under 5 minutes.

“Most regional banks have the capability, but the challenge for connectivity with instant payment schemes remains the wider adoption of gpi. For some of the local banks in Asia that are not connected to gpi, settlement is not happening within 5 minutes.”

When it comes to those domestic instant payment schemes, DB is positioning itself as a key regional figure with the launch of PromptPay instant payments in Thailand.

“PromptPay will facilitate instant payments in the domestic landscape on a real-time basis using proxy IDs instead of traditional bank numbers,” Shah said. “It is designed for retail-intensive industries such as telecoms, insurance and e-commerce that wanted to facilitate a 24/7 payment service for clients. Independent of SWIFT, it works on the domestic clearing system between banks.”

As part of the phase one rollout, the bank will be offering its clients instant collections throughout Thailand. Later in the year, phase two will enable instant payments to be made throughout the country.

Visa’s B2B Connect challenges SWIFT by addressing underserved segment

The system set to challenge SWIFT’s supremacy is Visa B2B Connect, the new global platform that the card giant built from the ground up using core assets and the latest technology to enable cross-border transactions directly between banks through a multilateral network.

It is seeking to fill the gap left by SWIFT, as it circumvents the correspondent banking network which is often the source of transfer delays, as most banks do not have direct relationships with each other.

Charlotte Le Gargasson,

Head of B2B Connect in Asia Pacific,

Visa

Rama Sridhar,

Executive vice president of digital and emerging partnerships and new payment flows,

Mastercard

Charlotte Le Gargasson, head of Visa B2B Connect in Asia Pacific, said that the product gives financial institutions a simple, fast and secure way to process non-card, high-value B2B payments globally.

“Today, high-value cross-border payments happen on a bilateral basis. Financial institutions need to establish relationships with corresponding banking partners and maintain a large global infrastructure. In this instance, payments are routed through bilateral correspondent bank relationships, passing through a varying number of intermediaries before reaching the beneficiary bank,” she said.

Visa B2B Connect was launched in more than 30 markets in June 2019, growing to 73 markets today. Le Gargasson said that Connect aims to be in over 100 markets by the end of 2020, and expects to reach 1 million transactions by 2021 as well as network scale by 2022.

“With Visa B2B Connect, we provide a single, multilateral connection to all network members where payments and data can move directly from one financial organisation to another. This approach allows for greater transparency, visibility, rich data and increased speed, all at a lower cost. In doing so, we are able to simplify the cross-border payments process significantly,” she added.

Mastercard looks to Real-time Payment strategy for its tech stack

Mastercard’s 2017 acquisition of bank account-based technology service Vocalink has signalled the card giant’s intention to move into the transfers market. Rama Sridhar, executive vice president of digital and emerging partnerships and new payment flows for Mastercard Asia Pacific, said that this fits into their broader real-time payments strategy.“Vocalink is now integrated into the broader Mastercard technology stack. We acquired it to give us the capability to seamlessly move from card rails to account rails, back and forth in all the services that we offer to the end consumer or to our client partners,” she said.

Sridhar added that across all emerging markets, the singular narrative is digitisation, and real-time payments is the key driver in markets where smartphone penetration outstrips the banked population. She also noted that a key differentiator is that Vocalink is already ISO 20022 enabled.

Mastercard is using Vocalink as the technology powering domestic market schemes such as InstaPay in the Philippines and PromptPay in Thailand.

“The Philippines is an interesting example. The government is trying to move from around 30 to 35% banked population to a target of 70% by 2023. For that to happen, there needed to be complete interoperability in the marketplace because you cannot have singular wallets operating within their own ecosystems. Real-time payments enable ecosystems to start being open, because you can fund from anywhere, and you can send to anywhere.”

The Philippines has one of the largest remittance markets in the world. Sridhar said that there are over 20 million GCash wallet accounts, and some 8 million PayMaya users that can be brought into the financially included segment from a transaction perspective.

In order to complement these existing domestic services, Mastercard in 2019 acquired cross-border payments company Transfast which it calls a “parallel service” to SWIFT’s offerings.

“In doing this, and establishing partnerships with cross-border payment providers such as Western Union and HomeSend, we are effectively opening up distribution points across as many markets as possible.”

Interestingly, while Sridhar noted that most markets in the region look fairly similar to the Philippines, the exception is Laos, where they have a higher wallet population than banked population. Still, most of these markets are expected to see a similar adoption curve, though the Philippines and Indonesia are expected to see a significantly higher volume of corporate disbursements, dividend payments and high-value payments.

Mastercard is keen to emphasise that in both domestic and cross-border payments, it is offering the same governance security and data management principles from its card rails now to its account rails.

“We are not a software vendor — we not handing out an RTP platform and walking away,” Sridhar said. “We are bringing together an ecosystem for RTP to work, which includes governance structures, helping the market understand commercial value exchange, and introducing a whole set of security services to be implemented simultaneously to secure the transactions. We offer the infrastructure with a much less upfront capital load on many of these countries, because that in itself could cripple adoption across the banking sector.”

Banking on APIs to bring large regional players back into the fold

Dhiraj Bajaj,

Head of financial institution sales,

Global transaction services for Asia Pacific

Bank of America

Benjamin Wong,

Co-founder and CEO,

TranSwap

Dhiraj Bajaj, head of financial institution sales, global transaction services for Asia Pacific at Bank of America (BOA), said that Asian banks who have been “active adopters” of SWIFT gpi are already seeing the benefits.“These banks are now able to demonstrate that 45% of their cross-border payments on gpi are settled within a few minutes, and around 95% are settled within a day. This is aiding SWIFT in building a case that SWIFT gpi is the long-term solution for demonstrating efficiency when it comes to cross border wire payments,” he said.

Bajaj pointed out a key trend over the last 12 months with how banks leverage the tracking capabilities of gpi and pass that on in real time to clients through their proprietary online banking apps — like one would an Amazon package. The next challenge to push back against fintechs in the cross-border payments space is using transparency to provide a better customer experience.

“The issue we are talking about with most of our clients — the reason why many customers migrated their cross-border payments to non-bank channels for smaller value transfers — was lack of transparency on fees and FX, speed of execution, and taking days to resolve queries on wire transfers where the beneficiary claimed non-receipt of funds,” he explained.

Borderless accounts seek to cash in

With the advent of transparency and tracking ability backed by SWIFT gpi, the trend in Asia over the last two years is banks offering an end-to-end FX payment solution. Bajaj said that as banks try to recapture the FX value proposition from fintechs, they are increasingly turning to BOA’s end-to-end API payment solution, which is going to substantially reduce reliance on nostro accounts — not to mention the compliance requirements involved in maintaining them.

“An end-to-end FX payments solution enables banks to close nostro accounts in currencies with minimal payment volumes and make their US dollar account with Bank of America their primary account and service their clients for payments in 140 plus currencies, backed by an online or digital experience.”

He believes that the changes will ultimately reshape the Asian banking landscape in favour of the larger regional players.

“Banks with a technology focus and budget, aimed at enhancing their client experience on payments, are able to gain volumes from the smaller banks — as well as get back the volumes on low value cross-border payments that had cannibalised to non-bank payment service providers,” Bajaj said.

This solution enables banks to retain their customers, their cross-border wire transfer payments, as well as retaining the fees and FX within banking channels.

“Over the last 15 to 20 years, banks would open 30 or 40 foreign currency nostro accounts,” Bajaj added. “With due diligence standards going up globally, it is a significant challenge for banks to complete annual KYC refresh on these accounts, involving a significantly large-sized administrative and compliance team to fulfil these requirements.”

Into this space, we are seeing the entry of exciting new players. Traditional banks such as Citibank have begun offering products such as Citi Global Currency Account, while foreign remittance fintech TransferWise has also begun offering a ‘borderless account.’

In Asia, home-grown cross-border business payments platform TranSwap launched its Global Borderless Virtual Account (GBVA), allowing business customers to open bank accounts in these locations virtually.

Benjamin Wong, co-founder and CEO of TranSwap, said they are currently licensed and operating in Singapore, Hong Kong and Indonesia. They are also launching the GBVA in the United Kingdom, Europe and US in May and June.

“Our goal for the GBVA is to allow businesses to effectively create and manage their own global treasury where they can hold money in 34 currencies and pay to over 180 countries,” he said. “We can help them create these accounts remotely, without physically travelling to the country to open the account. Of these, 89 countries can be executed through local ACH payment rails, making it cheaper and faster, while the GBVA is integrated via APIs to TranSwap’s global cross-border payment cloud platform, providing a single interface for multiple currencies.”

Wong added that once all required documents have been successfully submitted, an account can be opened within one hour on average.

“Users are able to register online for an account through our website and provide their basic information. Next, they will need to provide us with further details as well as a valid ID. During the sign-up process, a dedicated account manager is assigned to customers when they first register to provide any additional assistance. Once the account is successfully verified, we will notify the customer and they will be able to start using their Global Borderless Virtual Account.”

TranSwap adopts a stringent compliance culture and does not operate to sanctioned countries or high-risk industries, such as arms and ammunition, shell financial institutions, gambling and the adult industry.

“We are able to open accounts for individuals too, however our business model is more focused on corporate customers. Our plan is to have licences in 20 countries within the next three years.”

Blockchain shows that data may be the real battlefield

SWIFT has had rapid innovation to catch up on FX transactions, and the Society seems to have learned that it needs to be at the forefront of the next big revolution in payments: blockchain. The development of blockchain capabilities have changed the game when it comes to speed, cost and data potential.

Blockchain provider R3 is one of those leading the charge for the next generation of payments systems moving towards a trusted decentralised system. These systems use distributed ledger technology as opposed to a central clearing and settlement platform such as ACH or RTGS. Everyone – from national governments to big banks and SWIFT – is getting in line to reap the early benefits of blockchain’s potential.

Amit Ghosh,

Head of Asia Pacific,

R3

Alan Ko,

Head of fintech innovation at Tencent

Amit Ghosh, Head of Asia Pacific, R3, is ready to declare its collaboration with SWIFT on the platform Corda Settler a huge success. “We see payments as an area where blockchain has the potential to make the biggest impact as an efficient technology, saving costs and time,” he said. “Payment processes are still hindered by legacy technology that is cost, time and labour intensive. Blockchain can address these challenges.” While much of the advances to date have been in giving companies a new, fast, secure and reliable way to move crypto and traditional assets on a distributed ledger, another exciting application for blockchain is in the management of digital identities in the payments sphere.

“R3 has developed the underlying technology for self-sovereign identity that is transferable to many different use cases, including payments,” Ghosh added. “For example, when different payments companies need to verify identity, the siloed nature of their systems means this is complex, labour-intensive and cost-heavy. Using a blockchain-based digital identity system enables identity to be verified without requiring the mass duplication of identifying data, streamlining processes and adhering to privacy regulations.”

But as with any new technology, one of the key challenges is getting participants to embrace blockchain and to move away from well-established legacy systems. Cross-border payments is one area in particular that faces numerous compliance hurdles for new entrants.

“It is imperative that new technologies are developed in close dialogue with regulatory bodies. To that end, R3 has always actively engaged with regulators and government entities, inviting them into relevant trials and enabling them to observe and participate in the development of Corda. This has allowed us to understand what they are concerned about, and for regulators to understand what we are trying to do,” he said.

As for new products and services, Ghosh said that R3 is putting considerable resources into the Asian market, citing its particular involvement in the Monetary Authority of Singapore’s Project Jasper-Ubin and the Bank of Thailand's Project Inthanon.

“Asia is a hub for the trade of valuable digital assets and as such, the region has become a focal point for R3 to work with national regulators on how digital tokens might integrate into their regulated financial markets. We expect to see a lot more development in the area of digital assets, not just in Asia, but globally.”

Doubling down on the domestic front

If banks reclaim the FX space, smaller domestic players and fintechs are going to double down on domestic payments markets. Instant ACH infrastructure and the emergence of digital wallets have already seen a range of new services and products, such as microcredit to the unbanked. Bringing these consumers online will have numerous benefits in everything, from retail spending to remittances.

We have seen LINE Pay and GrabPay looking to replicate some of the success of Chinese giants Alipay and WeChat Pay, while a slew of new companies caters to domestic markets, such as TrueMoney in Thailand, GCash in the Philippines, Ovo and GoJek Pay in Indonesia, and MoMo in Vietnam.

Alan Ko, head of fintech innovation at Tencent, says that they are not worried about the competition. WePay is comfortable that it is well ahead of the pack, noting that their payments platform already has stability and scalability of the system, continuous innovation, and solutions for costs — not to mention that within this architecture, they must address the challenges of KYC, AML, FX, digital identities and e-wallets. “We developed our own distributed architecture and robust micro-core based banking systems based on commodity hardware and open source technologies, which not only can support the rapid growth of our business, but also keep our cost low enough to serve our long-tail customer base and maintain a sustainable business,” he said.

WePay clearly still has its sights set on traditional banking models, such as BOA’s vaunted new FX API, maintaining that open banking is the key to fostering innovation. Indeed, WePay has adopted the mantra of “the three opens” – open platform, open innovation and open collaboration.

“When it comes to open platforms, we need to go beyond API banking by sharing data models, algorithms, customer onboarding procedures, risk management and other capabilities with participants in the collaborative business ecosystem,” Ko added. “Financial services can be provided by retailers, non-financial service companies, fintech companies and software companies using API, SDK, and H5 provided by open banks like WeBank.”

Huge potential in tying in services with the payments market

Any emerging cross-border platform needs to be able to speak to the likes of WePay and AliPay as it does to any traditional bank. The money is talking loudly, with the global mobile payment market currently estimated at $816.5 billion, and projected to reach over $5.5 trillion by 2025.

Already, we’ve seen the next evolution cycle on from digital identities and e-wallets with the introduction of multi-currency wallets, such as Revolut and Youtrip, allowing consumers to use them across different countries at the lowest FX rate possible. One fintech firm, Geoswift, is going a step further. GeoswiftX, its cross-border payment platform, is providing a bridge across global payments ecosystems.

Raymond Qu,

Founder and CEO,

Geoswift

Fernando Restoy,

Chairman,

Financial Stability Institute

Bank for International Settlements

“The platform is a service,” said founder and CEO Raymond Qu. “It includes five functions: collection, geo-settlements, geo-remittances, geo-FX, and geo-card. Put the five together and then give our clients the flexibility to choose which they need.” Geoswift is generating around $10 billion in annual transactions across B2B, B2C and B2B2C in e-commerce, education and travel. One of its core businesses is accepting foreign tuition payments from students — largely from China, Korea, Japan and Hong Kong — and providing a one-stop solution to bridge the gap with what international schools are accepting, which is often only Visa and Mastercard. It is able to use the particular data it generates in these transactions to build out services for a mobile customer base.

“Big data plays a very important role in our business. We use it to tell where the market is, and what is the trend,” Qu added.

“In terms of cross-border payments, we have retail FX licence in China, and every day there are thousands of travellers in and out of China who need to get foreign currencies. With that data, we can do analysis and see where they are going to, when, the average amount they’re spending. It helps to not only understand the market, but to build new cross-border services to service the travel sector, such as partnering with Booking.com.”

He believes that the future is not just in the services you provide, but how you provide them. “People need to think beyond mobile wallets,” he said. “Using facial recognition or voice is very hot in China right now; people want anything that doesn’t involve touching screens.”

Governments remind finance that the world still has borders

As banks move swiftly to keep up with payments innovators, so too are regulators. Central banks around the world are considering how they will need to adapt their supervision regimes that will only continue to grow in size.

States are beginning to think about flows of money and systems moving beyond their control, threatening their ability to regulate and control, and in the longer term, potentially even having an effect on national economic policy.

While SWIFT may be applauding its multinational banking collaboration efforts, the same cannot necessarily be said for governments. At a time when the world’s payments infrastructure is increasingly moving across borders, politically we are in an era of mounting protectionism and nationalism. There is no guarantee that cooperation will be forthcoming.

That said, regulators are certainly aware of the need for collaboration.

Fernando Restoy, chair of the Financial Stability Institute of the Bank for International Settlements, said that the case for international standards is already strong in some areas such as data management.“While central banks can contribute to promote an adequate regulatory response at the domestic and the global level, it is clear that this should be the result of a multi-disciplinary effort in which other policymakers — including competition and data protection authorities — also have a prominent role,” he said.

It remains to be seen, however, how much this thinking is tied to 20th century ideas of political and financial blocs, with news that China, Russia and India are exploring a “gateway” model for messaging systems in developing countries in an attempt to work around American sanctions.

Collaboration is key in the payments ecosystem

While COVID-19 has accelerated an already strong trend away from paper-based payment products, such as cash, cheques, and vouchers, it has brought into sharp focus the products that will replace them. For consumers and businesses alike, we expect to see a continuing upward trend in the adoption of all things digital.

Existing payment providers are expected to merge payment forms within product offerings, such as a debit or credit card with contactless payment and a digital wallet option. QR codes are likely to continue to outstrip NFC technology due to the established popularity of QR codes in Asia, though digital giants such as ApplePay and SamsungPay will be trying to change that.

The changing global payments system is one with many faces. Financially, borders are becoming less of a barrier to the movement of money, yet rising political nationalism within those borders will continue to pose a challenge for businesses, regulators and governments alike. At the same time, transformative innovation is seeing exciting opportunities open up for partnerships between those doing the disruption and the market’s traditional powerhouses. Yet, seemingly distinct challenges point to the same principle: collaboration, not collision, is key to success in these global payments ecosystems, whether between new entrants and incumbents, or regulators working across borders.

.png)

.webp)