- From technology and commercial perspective, payment is no longer a revenue game for banks

- With the reduced margins there is a need to look at more creative areas to identify revenue opportunities

- To be successful, institutions need to innovate the technology infrastructure, improve agility and cost efficiency, and adopt strategies and models that can deliver future value

The payments ecosystem has shifted dramatically towards instant and frictionless payments. Asia Pacific region witnessed a spurt in digital wallets, mobile payments, e-commerce transactions and digital ecosystems. Several countries in the region developed national real-time payment infrastructures harnessing the growing adoption of smartphones, digital IDs and quick response (QR) codes. Developments in the Society for Worldwide Interbank Financial Telecommunications global payments innovation (SWIFT gpi) and ISO 20022 added to the transparency and speed in cross-border payments. Meanwhile, the events of 2020 proved to be a catalyst that accelerated digitisation and contactless payments.

As consumer expectations evolve, institutions are forced to rapidly upgrade the fragmented legacy systems and data architectures. Wider payment services through open banking framework and digital ecosystem offer new customer engagement opportunities. Shrinking payment margins and revenues drive institutions to explore incremental income streams, monetise data insights to expand customer offerings and explore embedded financing options such as buy now, pay later (BNPL) and supply chain financing. The BNPL model is poised for exponential growth as volumes surge and new fintechs and institutions expand their market reach.

Real-time payments and digital volumes grow multifold

Fintech and tech players gained market share with their propositions in ‘anytime, anywhere’ payments through innovative peer-to-peer (P2P) payments, digital wallets, QR payments, and point of sale services. Customer expectations and behaviour shifted from cash to instant, digital and 24/7 payments. Smartphone, internet penetration and e-commerce growth are driving the need, speed, and pace of change.

Financial institutions (FIs) found it difficult to match the agility and transparency of nimble technology players in capturing the growing small value payments. WeChat Pay acquired 800 million monthly active users, Alipay has 731 million users, and Apple Pay has around 450 million users while new superapps emerged such as Grab and Gojek in Asia.

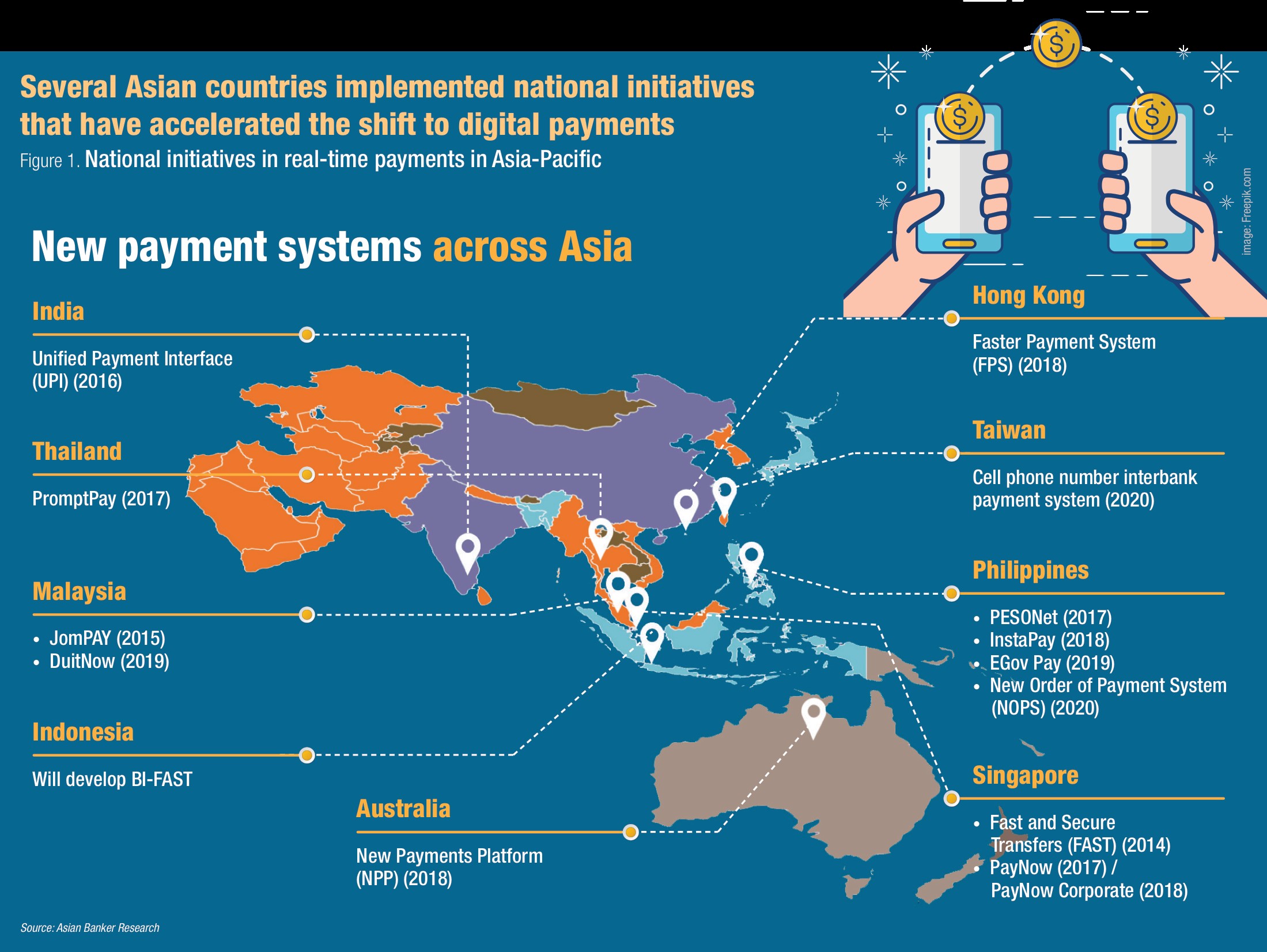

India launched Unified Payment Interface (UPI) in 2016 that has seen significant success. Other initiatives include Singapore’s Fast and Secure Transfer (FAST) system, Thailand’s PromptPay, Malaysia’s Duitnow, Hong Kong’s Faster Payments System (FPS) and the Philippines’ InstaPay. Meanwhile, USA and UK are creating overlay services like request to pay.

In Asia, India witnessed the highest daily real-time transactions at 41 million payments per day. The Philippines has the highest increase in payment volumes in the past year at 309% followed by Australia (214%), and India (213%), according to the payments report, Flavors of Fast 2020, released by Worldpay from FIS.

Digital volumes continue to climb. Citi research forecasts that digital forms of payment including wallets, instant payments and cards will comprise over 90% of the growth in consumer-to-business (C2B) payments by 2021. Meanwhile, the 2019 e-Conomy SEA report by Google, Temasek, and Bain & Company estimated that digital payments will exceed $1 trillion in transaction value by 2025.

“There is a mix of disintermediation and a long tail of transactions coming into FIs which never existed before, because of QR, waving credit cards and government initiatives. A large number of minute micro transactions are coming into the ecosystem and the volumes are going up. The real disintermediation is the customer getting lost to these wallets and other providers upfront,” said Kanag Surendran, managing director and head of transformation at CIMB.

Kanag Surendran,

Managing Director and Head of Transformation,

CIMB

Lito Villanueva,

Executive Vice President and Chief Innovation and Inclusion Officer, RCBC

Kanag Surendran, Managing Director and Head of Transformation, CIMB

Acceleration to contactless digital payments became more pronounced during the pandemic as customers shunned cash.

“In the Philippines, amid the pandemic, we have seen the exponential growth of digital transactions due to limited mobility. We have seen that numbers are skyrocketing. For example, in RCBC we’ve seen three to four-digit growth in digital transactions,” shared Lito Villanueva, executive vice president and chief innovation and inclusion officer, RCBC.

Lito Villanueva, Executive Vice President and Chief Innovation and Inclusion Officer, RCBC

The e-commerce volumes and digitisation of small offline merchants surged during the pandemic as consumers shifted towards online sales.

Cross-border payments become more transparent and efficient

Cross-border payments have traditionally been opaque, expensive and subject to delays with regulatory compliance challenges. Asia is characterised by multiple domestic payment systems having a different level of development, regulations and currencies leading to interoperability issues. However, there are now growing bilateral real-time payment arrangements. For instance, by mid-2021, users of PayNow in Singapore or PromptPay in Thailand will be able to send money across two countries using their mobile numbers. Thailand and Cambodia are implementing a QR-based payment infrastructure for retail payments across two countries.

Industry-led developments of SWIFT gpi and ISO 20022 addressed some of the existing challenges by adding speed and transparency in high-value payments across institutions. Global adoption of data-rich ISO 20022 messaging standards is expected to improve payments efficiency and streamline communication across FIs.

“SWIFT gpi provides transparency in tracking a transaction and getting the right level of inputs on conversion rates, foreign exchange (FX), and charges incurred across multiple nodes. At the back end, legacy platforms need to change to accommodate that. That is one of the reasons why we see that only selected banks are on SWIFT gpi across 30,000 financial institutions that do transactions through SWIFT,” said Venkat ES, head of Asia treasury product, global transaction services, Bank of America.

Venkat ES,

Head of Asia Treasury Product,

Global Transaction Services,

Bank of America

Michael Moon,

Managing Director,

Payments and Trade Markets,

Asia Pacific,

SWIFT

Venkat ES, Head of Asia Treasury Product, Global Transaction Services, Bank of America

SWIFT’s gpi instant payments service combines gpi features with domestic real-time payment networks, rendering cross-border payments faster and seamless. The ISO 20022 is likely to improve the data access to institutions.

Michael Moon, managing director, payments and trade markets, Asia Pacific at SWIFT, explained, “All of the transactions, where possible, will be done on an instant basis and friction-free. It is about identifying the problems and frictions that exist at scale in the industry and helping the industry by centralising services such that the cost burden is not duplicated across individual banks and it can be shared”.

Michael Moon, Managing Director, Payments and Trade Markets, Asia Pacific, SWIFT

SWIFT is now piloting with banks for low-value retail cross-border payments towards predictable, faster payments with real-time status tracking. Developments by SWIFT and industry participants not only improve the competitive capabilities of banks but also change the revenue dynamics.

“A big change happening with our clients is the adoption of application programming interfaces (APIs) and moving away from proprietary communication channels. Real time payment (RTP) systems that operate 24 hours a day, 365 days a year will enable gpi instant in many markets over the years. The important differentiator is that for a merchant, there is no interchange paid on RTP so you use the card volumes in the future. In cross-border, it has a huge impact on the FX and the interchange when you use an RTP infrastructure versus a card,” elaborated Dhiraj Bajaj, head of Asia Pacific FI and NBFI Sales, global transaction services at Bank of America.

Dhiraj Bajaj,

Head of Asia Pacific FI and NBFI Sales,

Global Transaction Services,

Bank of America

Chintan Shah,

Asia Pacific Head of Corporate Cash Management,

Deutsche Bank

Dhiraj Bajaj, Head of Asia Pacific FI and NBFI Sales, Global Transaction Services, Bank of America

Institutions seek to form new linkages that can provide alternatives to inefficient nostro/vostro routes in multiple corridors such as Visa B2B and Ripple.

Selected countries are also exploring Central Bank Digital Currencies (CBDC) which could improve efficiency and interoperability in cross-border payments. The Hong Kong Monetary Authority (HKMA) and the Bank of Thailand collaborated in May 2019 for Project Inthanon-LionRock to study the application of CBDCs in cross-border payments. The Bank of Canada and the Monetary Authority of Singapore (MAS) also conducted trials on cross-currency payments using CBDCs.

Technology transformation is critical to accommodate rapid industry changes

The customers increasingly expect real-time payments but many banks are still saddled with slow siloed legacy systems. These are not geared for 24/7 services, have a high operating cost base and fragmented architecture. Meanwhile, the regulatory compliance obligations have become more complex across real-time and cross-border payments. It is now critical for banks to upgrade their legacy back end architecture and systems for real-time services, open banking and scalable architecture.

“We worked on building our payments infrastructure to cater to large volumes of low-value payments compared to simpler forms of vendor payments earlier. Second, we needed to adapt to a greater 24/7 infrastructure across the region. We migrated the entire routing logic from channels into our payment lifecycle management layer. On the cross-border payments, we have continued to invest in our FX and cash engine and on integrating payments, FX and liquidity solutions on a single front to back solution for our clients which digitises payments,” shared Chintan Shah, Asia Pacific head of corporate cash management at Deutsche Bank.

Chintan Shah, Asia Pacific Head of Corporate Cash Management, Deutsche Bank

Venkat ES said the focus is to get the foundation and core banking right, technology transformation in place as the bank joins the real-time payments, ISO 20022 or SWIFT gpi. “The analogy is that it is almost like the mid-air refuelling exercise between two flights,” he added.

The key challenge for banks is how to achieve real-time treasury capability. This requires an integration of multiple back end systems as well as real-time visibility into the customer balances, credit analytics and currency liquidity positions.

“The strategy that most banks are adopting is towards a universal model of different payments through the ecosystem,” argued Bajaj.

Institutions are expanding ecosystems, fintech partnerships and open banking frameworks through APIs to have wider service offerings to retain customers and data access. However, they need to reassess the data architecture and integrate systems to have effective insights.

“With growing micropayments, the challenge is on the scalability. Currently, we are trying to create banking as a platform and enable fintechs and some of our third-party partners to use our payment infrastructure and leverage our platforms. The usefulness of payments is more on the data. So, we are now trying to enable streaming in real-time,” said Trirat Suwanprateeb, EVP, head of technology and operations at Siam Commercial Bank.

Trirat Suwanprateeb,

Executive Vice President,

Head of Technology and Operations,

Siam Commercial Bank

Dennis Omila,

CIO,

Union Bank of the Philippines

Trirat Suwanprateeb, Executive Vice President, Head of Technology and Operations, Siam Commercial Bank

Pandemic accelerated the push towards ecosystems and opportunities of collaboration while the need for large offline and physical networks shrunk. Institutions collaborate with fintechs to expand the payment services, explore new opportunities and grow the settlement volumes. In Asia, Siam Commercial Bank partnered with Ripple Net. Krungsri Bank partnered with NTT data to launch QR code payment in cross-border payments. UOB tapped Visa API and its partnership ecosystem to simplify digital payments.

Revenue drivers and evolving strategies

Industry developments resulted in new challenges and opportunities for institutions. Margins have been squeezed and the need to improve cost efficiencies has become critical. But with the digital ecosystem, there are new opportunities to grow scale, improve customer relationships and monetise data to implement new business models in payments.

“From a strategy point of view, the first is to create the scale in payments. Secondly, look for new business models with existing customers like e-commerce or subscription economy. People shifting their payments from credit cards to real-time payments could give a significant upstream. The third aspect is to look for a new value proposition. Finally, the enhanced adoption of technology, almost 100% straight-through processing, can facilitate to bring down the cost significantly. High-tech and low touch are going to drive the strategy in the future,” explained Venkat ES.

“We want to make sure that wherever the customer wants to pay for his goods or services then we are there as a choice. From technology and commercial perspective, payment is no longer a revenue game for banks. The real value is in trying to ensure the technology and operations are so streamlined that your cost of providing that payment at scale is as minimum as possible and the fraud losses are kept minimum,” said Surendran.

With the reduced margins there is a need to look at more creative areas to identify revenue opportunities. Venkat ES said the three key components of payments evolution are send, lend and mend. “Lend - how do we build the financing options using the payment capabilities that are coming in a big way like the BNPL, supply chain finance solutions, and personal finance solutions? Mend is a combination of data analytics, artificial intelligence and machine learning that is still evolving but also coming in a big way.”

Payments bring wider data insights along with the natural opportunity to build end-to-end engagement with customers. Fintech and challenger banks can utilise this data effectively for incremental revenue.

Dennis Omila, CIO, Union Bank of the Philippines

Transactional data provides fintech companies with additional insights to offer varied loans and enable new revenue stream.

During the pandemic, digitisation of merchants and online sales has increased. “As online sales volumes increased, we help online merchants through a very simplified process which allows them to accept payments from different modes. We’re getting a lot of traction there and have onboarded many online merchants in our ecosystem,” said, Dennis Omila, CIO, Union Bank of the Philippines.

Buy now, pay later poised for growth

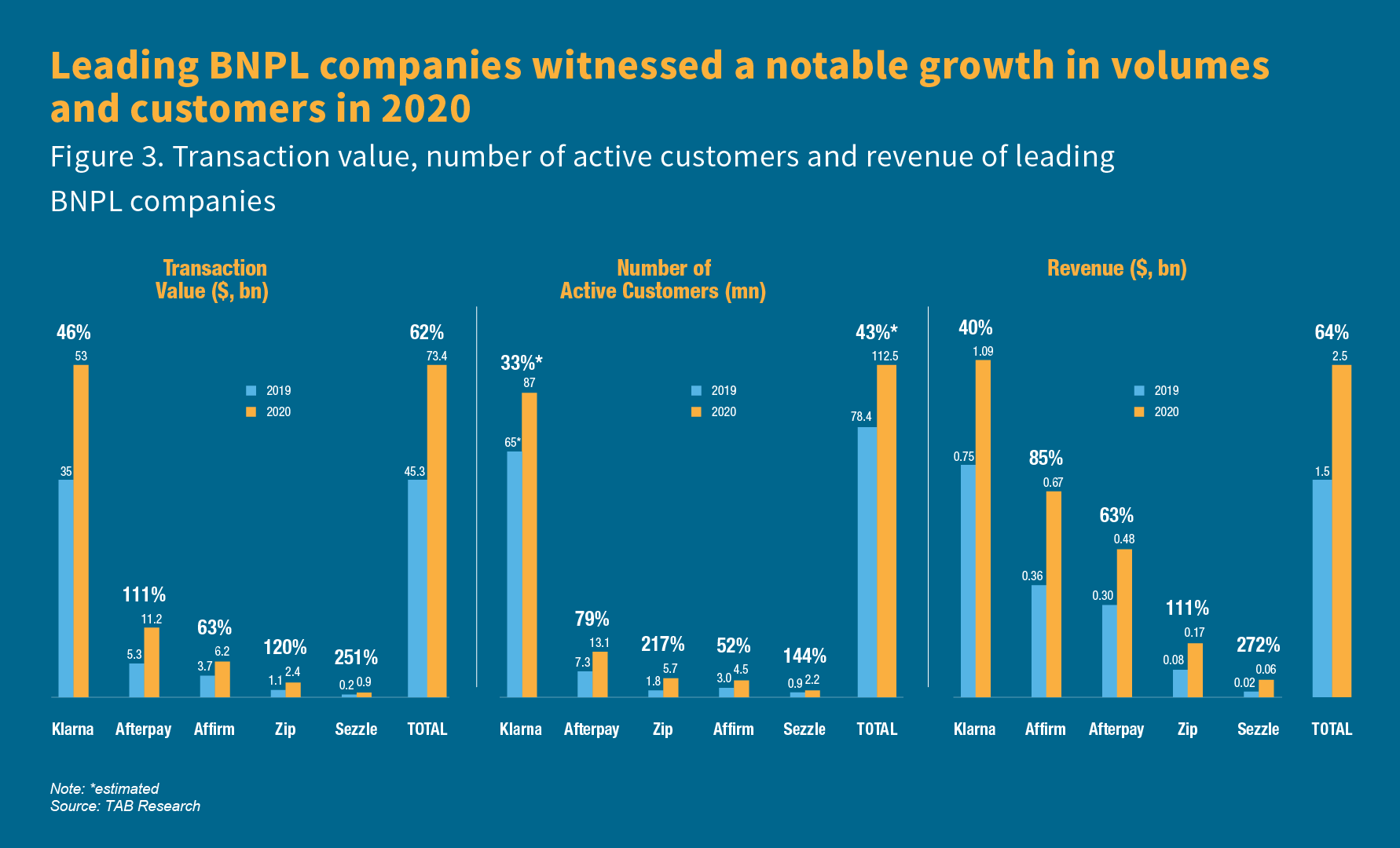

BNPL is revolutionising the online payments and payments ecosystem. It widens the choice for customers that enable them to purchase goods through transparent credit or instalment while it improves the check-out rates, transaction value for merchants and their ability to attract customers. BNPL had a notable growth in the last few years but the volumes shot up further during the pandemic as online shopping surged and the demand for short-term credit increased.

Globally, the valuations for some BNPL companies skyrocketed. For example, Swedish company Klarna grew to become one of the highest-valued companies in Europe. It claims to process over a million transactions daily and it has 90 million consumers across 200,000 merchants in 17 countries. Australia-based AfterPay had a 112% increase in sales in fiscal year (FY) 2020 as it expanded its reach in US and UK markets. US-based Affirm raised money in an initial public offering (IPO) with an implied valuation of $12 billion. The success of these leaders is motivating the entry and funding of several other new players.

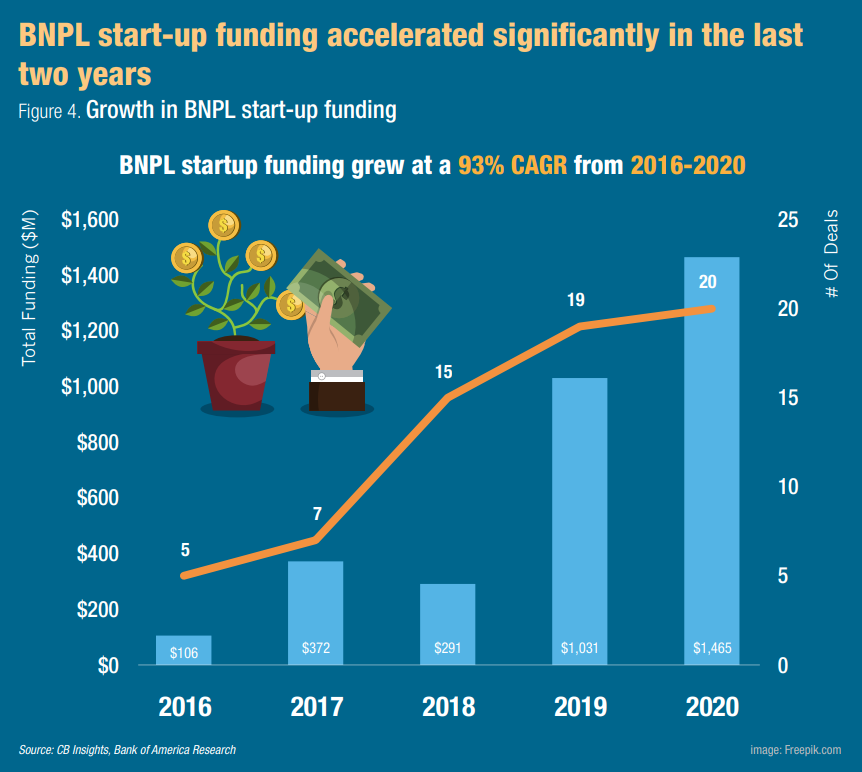

According to Kaleido Intelligence projections, $680 billion will be spent by global consumers using electronic point of sale (ePOS) finance/BNPL over e-commerce channels in 2025, a rise of 92% over the $353 billion spent in 2019.

Several financial institutions are now launching BNPL services for customers. Visa, Mastercard and American Express have all entered BNPL space. The Commonwealth Bank of Australia partnered with Klarna. Goldman Sachs launched MarcusPay that allows users to divide big-ticket purchases into monthly payments. Citi Australia launched a new offering with online retailer Kogan.com which allowed Citi credit cardholders to opt for BNPL at checkout. UOB launched SmartPay converting bills into interest free monthly instalments for a fee.

PayPal launched the BNPL option to pay in instalments in the US and UK in second half of 2020. This service witnessed a notable growth and the company reported over $750 million payment volumes across 2.8 million customers in the fourth quarter of 2020 (Q4 2020).

BNPL growth across markets

Many markets such as the US, UK, Sweden and Australia have witnessed strong growth in BNPL. In the UK, BNPL products nearly quadrupled in 2020 and were estimated at £2.7 billion ($3.75 billion) with five million people using these products since the beginning of the pandemic according to a Financial Conduct Authority (FCA) review.

Australian Securities and Investment Commission (ASIC) reported over 6.1 million BNPL accounts in Australia as of June 2019, representing about 30% of the country’s adult population and 56,000 merchant agreements across BNPL providers. The number of active accounts grew 38% to 3.7 million in 2018–2019 while the transactions increased 75% from 1.9 million in June 2018 to 3.4 million in June 2019.

Several new players are looking at Southeast Asian market. For example, Pine Labs, a merchant commerce platform from India, has expanded in the region in partnership with Mastercard.

“Consumers are saying that they will spend more if they’re given this option. The ticket sizes are expected to go up by 15% if that option is available to them. So, it results in higher ticket prices, less cart abandonment, and then more revenue for the merchants and the lenders,” explained Sandeep Malhotra, EVP product and innovation at Mastercard.

Sandeep Malhotra,

Executive Vice President Product and Innovation,

Mastercard

Amrish Rau,

CEO,

Pine Labs

Sandeep Malhotra, Executive Vice President Product and Innovation, Mastercard

Pine Labs plans to launch in Thailand and the Philippines in early 2021 followed by Vietnam, Singapore, and Indonesia. Pine Labs processes about $30 billion annual payments, serving about 150,000 merchants across 450,000 network points across the countries and claims to be a leader in offline BNPL services in India. It now plans to enable instalments via multiple channels like credit cards, debit cards and bank accounts across in-store and online merchants in Southeast Asia.

“Our payment technology can consolidate multiple credit issuers on a single platform which will be very relevant in Southeast Asia,” said Amrish Rau, CEO of Pine Labs. He added that the company experienced a 70% growth year-on-year (YoY) in ‘pay later’ products in India.

Amrish Rau, CEO, Pine Labs

Among other players, Singapore-based Razer Fintech and Rely announced a partnership to offer BNPL services to merchants. Other BNPL companies in the region include Gojek PayLater, Grab PayLater, Octifi, and Hoolah.

In Indonesia, the BNPL companies include FinAccel that runs the platform called Kredivo. Australia’s AfterPay reportedly acquired EmpatKali while other leading players include Akulaku and Ovo.

FinAccel’s CEO and founder Akshay Garg said, “In Indonesia, less than 10% of the eligible population has access to credit cards and we are primarily solving the problem of credit access. But in developed Western markets like the US or Australia, BNPL companies solve the problem of ‘convenience’ rather than credit access”. He claimed that his company has grown around 200% per year and plans to expand in other emerging economies in the region.

Akshay Garg,

CEO and Founder,

FinAccel

Peter Barcak,

CEO and Founder,

CredoLab

Akshay Garg, CEO and Founder, FinAccel

Varied business models

In developed countries, customers have access to credit cards but seek the convenience of transparent and interest-free credit which gets fulfilled by BNPL companies that offer a digital card equivalent model.

BNPL models generate income primarily from merchant fees but some may have interest income from consumers. Klarna primarily earns from merchant fees while Afterpay earns 80% revenue from merchants and the balance from late payment charges from consumers. PayPal does not charge an interest but has a late fee component. Affirm earns from interest income and merchant fees.

In countries like Indonesia, the model could vary as consumers may be more adaptable to pay interest on the financing. “Our revenue model is primarily from the consumer interest charged although we also charge a merchant fee. In emerging markets like India or Indonesia, the merchant fee-paying revenue model doesn’t work. The merchant fee revenue model works better in countries with high credit penetration,” explained Garg.

BNPL companies may not charge interest but may have a hefty late fee which becomes onerous for customers if they shore up credit beyond their repayment capability. This sector has remained in the regulatory blind spot. However, the demands for regulatory controls are increasing.

The Australian Finance Industry Association’s Code of Conduct for BNPL providers will come into effect soon. In UK, a review by Financial Conduct Authority (FCA) suggested the need to bring stricter controls for BNPL agreements. In Singapore, MAS is reviewing regulations for BNPL.

Credit analysis remains a key success factor in BNPL

A key differentiator for a successful BNPL will be the institution’s ability to do advanced credit analytics and control defaults. Fintech companies focus on the integration of multiple data sources in the ecosystem along with an advanced risk assessment engine and the use of machine learning and artificial intelligence (AI) algorithms.

In some emerging economies where the credit bureau data is limited, there is a greater need for proprietary data pipes and non-traditional data to develop credit scores. Several fintech companies target this segment.

For instance, Credolabs is a fintech that uses smartphone and web metadata to help lenders and businesses underwrite.

“A lot of BNPL players face the issue of significant data asymmetry between scorable and unscorable populations, lack of data and thin files from credit bureaus. We bring a completely new set of data that improves the overall predictiveness of the lenders’ existing models,” said Peter Barcak, CEO and founder, CredoLab. He added that as this data has little co-relation to the credit bureau and other traditional data, it provides a complimentary solution to get a 360 degree assessment of applicants.

Peter Barcak, CEO and Founder, CredoLab

Besides a strong risk assessment capability, other critical success factors for BNPL companies include access to multiple credit capital and funding partners, having a wide merchant network and the ability to provide a differentiated customer experience.

Outlook

The payment transformation and innovations are creating opportunities for new business models, collaborations and new customer experiences. As the margins in payments reduce, there is a growing urgency to monetise more data effectively to tap into incremental revenue opportunities. To be successful, institutions need to innovate the technology infrastructure, improve agility and cost efficiency, and adopt strategies and models that can deliver future value with a competitive advantage.

.png)

.webp)