- Banks have embarked on a digitisation of products and services to reduce their operating costs

- The integration of micropayments into messaging platforms like WeChat in China has driven digital payments

- Fintech startups entering into key retail financial services areas such payments and lending have forced banks to innovate and put their customers first

Banks are aware of the threats that are coming in the long term to disrupt their existing business models. The two classic competitive advantages of commercial banks – capital and physical presence – are proportionally becoming less relevant. Banks know they need to capture, demonstrate, or create value in the digital space – a field which requires a new kind of leverage and capabilities beyond the account centric banking relationship.

Digitisation of products and services

Many banks embark on the digitisation path with the goal of reducing “friction” in the customer journey and cutting operating costs. For example, opening a bank account in the Philippines typically takes an average of more than 60 minutes to complete, with up to nine different documents and more than 120 data fields to fill out. A paperless and fully straight through process (STP) is, for most but a few leading banks, a distant reality. Yet, things have been improving. Singapore-based DBS Bank and UAE’s ADCB have introduced full STP for approving personal loans albeit for existing customers. In Australia, more than 40% of Westpac’s credit cards are originated and sold online. ANZ in Singapore has developed a digital on-boarding programme for its Optimum Card. On the other hand, opening online deposit accounts among new to bank customers is increasingly becoming the industry standard in Australia.

Pure digital banks

Those initiatives, however, are incremental compared to pure-play digital banks, which are emerging globally and increasingly outside the US and Europe. In Asia Pacific, Jibun Bank, a mobile-only bank player in Japan, and Australia’s UBank were the earliest examples of spin-offs from larger banking groups. These banks found it easier to set up separate standalone digital banks instead of subjecting the entire organisation to the arduous and risky process of digital transformation. In fact, Jibun Bank attracted more than 500,000 new customers in its first year of operations. In 2015, the bank reported the highest number of mobile banking accounts in Japan – two million – growing at a compounded average growth rate of 11% between 2008 and 2015. The bank broke even in less than five years. It initially relied substantially on customer and product referrals from its parent bank, Bank of Tokyo Mitsubishi UFJ. Furthermore, its 200 headcount workforce was able to generate a revenue of $218 million in 2015. On a revenue per employee basis, it exceeded that of mobile-only bank Hello Bank! and online bank ING Direct Australia.

Pure digital banks are increasingly being established by non-bank entities. In late 2015, Korea’s leading messaging app KakaoTalk, and KT, one of the leading telecommunication companies, set up the country’s first Internet-only bank. In Vietnam, where 50% of people are regular internet users, Vietnam Prosperity Bank launched the country’s first mobile-only bank, TIMO, in early 2016. However, TIMO is not a 100% digital banking, as customers will still need to visit its TIMO Hangout location to open an account.

War on payments

Facebook was reported to be expanding its payment services in Asia, which will allow users to pay for products listed in Facebook pages similar to WeChat. According to reports, trials are currently being run in Thailand through 2C2P’s, an established cash and credit card payment processor founded in 2003. In Thailand, there are more people who have a Facebook account than those with bank accounts. Apple, Google, and Samsung have launched, at varying degrees, their payment wallets in Asia. However, they might remain less popular in emerging markets as they require credit cards, which are not always relevant for lower income segments. But still, they require basic banking and payment services. To reach out to these segments in Asia, fintech startups like Philippine’s Coins.ph, Vietnam-based MoMo and 1Pay, and Tapp, a Finland-based mobile payment company, are aiming to tap into existing micro cash payments without involving formal banking institutions. Tapp has already raised almost $12.9 million and MoMo has bagged a $28 million investment from Standard Chartered (SCB) and Goldman Sachs.

The convergence of messaging platforms and the integration of micropayments are powerful combinations best demonstrated by the success of WeChat’s e-payment services in China, which offers an integrated wallet that is compatible with all phone operating systems. The system also allows users to make payments without having to exit the WeChat app, which has a staggering 650 million users.

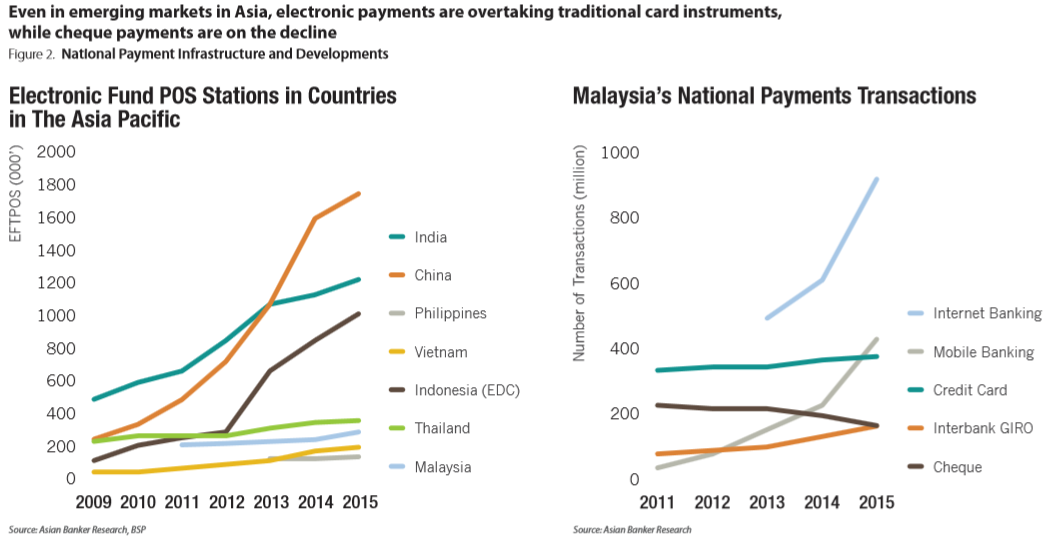

National e-payment infrastructure upgrades are being implemented in the UAE, India, Thailand, Malaysia, and the Philippines. It is expected to further drive digital payments adoption. On the other hand, China will open its national payments infrastructure to the global payment networks. However, the growing relevance of local and regional networks such as RuPay in India have challenged the dominant position of leading institutions like MasterCard and Visa in the local markets. In addition, Paypal acquired Xoom, a digital only remittance provider, and has ambitions to evolve beyond a mere processing factory to develop its own global payment network.

Biometrics and customer authentication

With the increasing adoption of online and mobile channels, the industry is witnessing a shift in fraud activities, which has been aided by the migration of card payments to EMV technology. Given the financial and reputational ramifications, banks have started implementing advanced technologies to combat cyber fraud such as real-time fraud analytics, geo-location tracking, biometrics, and mobile secure location in addition to existing authentication methods.

Blockchain and distributed ledger

While payment service is touted as a prime candidate for the application of blockchain technology, the potential implications go far beyond. It impacts back office systems and functions extending into security, risk, audit, underwriting, network reliability, and transaction efficiency and traceability. Nevertheless, it is still very early in the development cycle and may be some time away from any real world practical applications.

Fintech – not yet making a real impact on the market

While financial technology has entered board room discussions and banks have started pondering on potential collaboration with fintech startups, they are doing so with a certain degree of caution. Some leading banks in Asia Pacific are taking a conservative approach to improve both in-house capabilities and competitive market positions. Banks in China are taking a more proactive approach, given the direct competition from non-banks and fintechs. In the long run, fintech will not become a threat to the banking sector, especially when the best banks will have the ability to cooperate with them like any other network partners. What is worrying is the evolution of fintech startups that may challenge the turf of existing information technology (IT) and solution providers. These include startups that can grow their clout and expertise in collaboration with the banking industry.

Crowdlending

New developments in financial technology, the improved availability of public personal information, better internet bandwidth, minimal regulations, and underdeveloped or concentrated markets have given rise to alternative lending platforms. One of these is crowdlending, which connects lenders with borrowers without the intermediation of banks. Unlike banks, crowdlending platforms generally do not earn a margin on the loan, instead they charge fees. In 2015, around 2,600 peer-to-peer (P2P) lenders – representing 96% of the roughly 2,700 crowdlenders in the region – were based in China, where 98% or $113 billion worth of loans originated. However, since mid-2015, the net growth of crowdlending platforms began to slow, with the same number of crowdlenders coming into and exiting the market. Due to the inroads that crowdlending created in the retail lending space, banks started to adapt similar technologies and had shifted their focus to consumer and SME loans. It is expected that in the mid-term, crowdlending, as an alternative lending platform to commercial banking, will only grow in much defined niche markets that are unattractive to banks due to the lack of critical mass and/or risk profiling. Moreover, given the platforms’ low loan volume, achieving a sustainable and profitable business based on fee income only could be hard to achieve.

Digital transformation on a more fundamental level

As banks continue to improve their digital banking presence and speed-to-deliver, fintechs are forcing these same incumbents to address digital transformation on a higher fundamental level: how financial products are manufactured, distributed, serviced, and operated. Banks are currently challenged by how to sieve through the noise and address the genuine threats from fintechs, and how to integrate new technologies into their core businesses, while evolving their management model.

.png)

.webp)