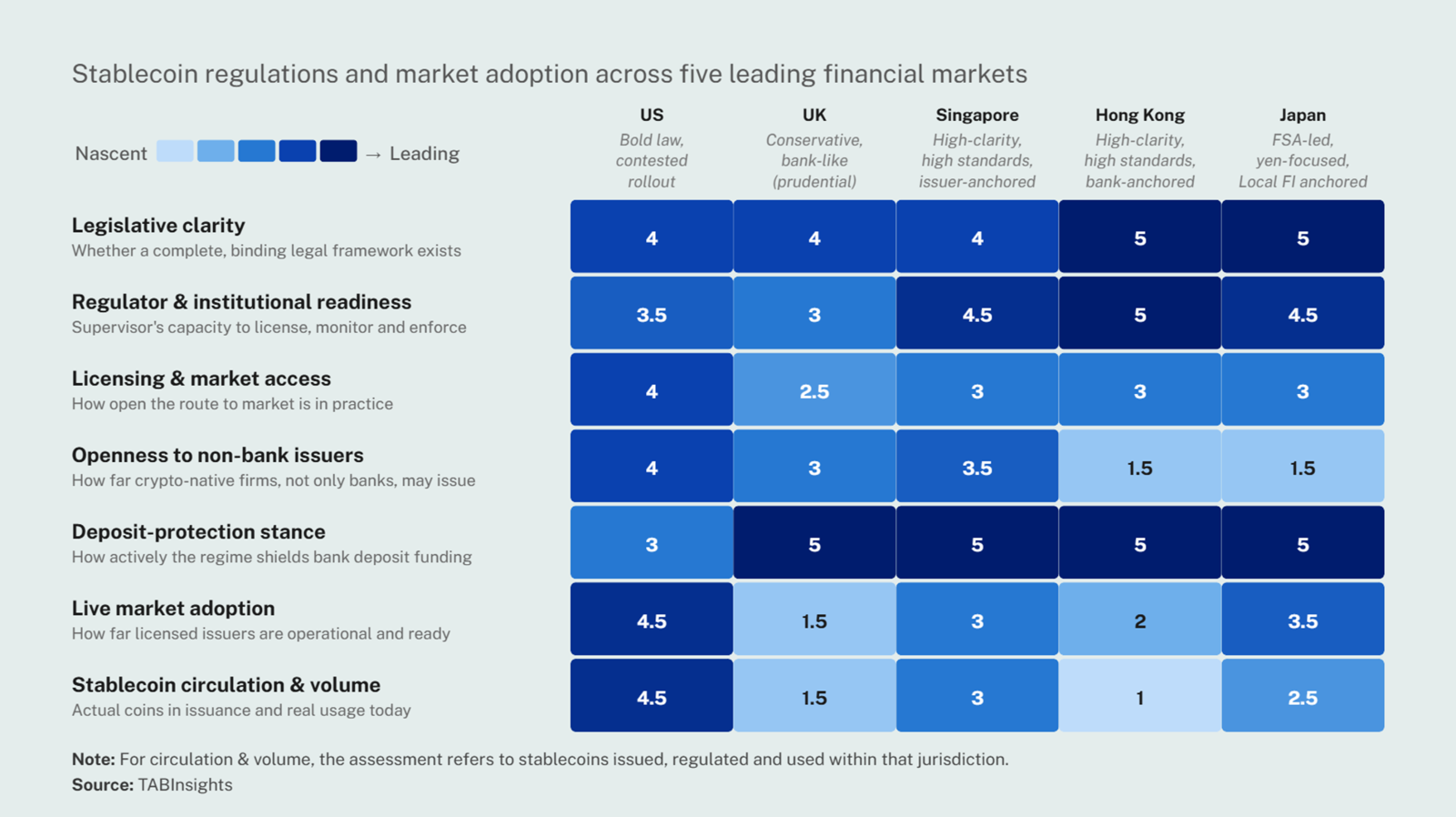

Over the past 2.5 years, these five jurisdictions have converged on a common regulatory foundation: full one-to-one backing with high-quality liquid assets, segregation of reserves under trust, redemption at par and broadly aligned disclosure standards. The debate over first principles is largely settled. The differences now lie not in what constitutes a stablecoin, but in how each jurisdiction manages the friction between stablecoins and incumbent banks. In every market, that tension remains unresolved.

The treatment of interest illustrates this tension. Both the US GENIUS Act and Hong Kong's Stablecoins Ordinance prohibit issuers from paying yield on stablecoins on the premise that interest-bearing stablecoins become substitutes for bank deposits. The United Kingdom reaches a similar outcome through structural safeguards, requiring systemic issuers to hold at least 30% of reserves in non-interest-bearing central bank deposits and capping issuance at GBP 40 billion ($54 billion) per stablecoin. Japan takes a different approach, embedding stablecoins within a tightly controlled licensing regime under the Payment Services Act, limiting issuance to banks, trust companies and registered money transfer operators. Singapore, meanwhile, tightly restricts what issuers may hold and do. While the mechanisms differ, the objective is the same: to limit deposit disintermediation and impose prudential discipline as stablecoins move towards systemic scale. Central banks, including the European Central Bank (ECB), now explicitly warn of liquidity run risk and spillovers into sovereign bond markets and payment systems, underscoring a broader shift from permissive oversight to financial stability-first regulation.

This has created a clear jurisdictional divide among the world's leading stablecoin markets. The US remains market-led and politically driven. The UK takes a prudential-first approach, moving towards bank-like regulation for systemic stablecoins. Singapore is issuer anchored, combining strict reserve and redemption requirements with controlled innovation. Hong Kong has adopted a licence-based, bank-anchored model with rigorous compliance standards. Japan, meanwhile, permits distribution only through local financial intermediaries and is steering the market towards a JPY-centric stablecoin regime.

The US legislates boldly, but is politically the least settled

The US leads on live adoption, circulation and market access, with dollar-denominated stablecoins already transacting at scale and an open charter pathway for issuers. While US dollar stablecoins account for more than 90% of the $315 billion global market, no verified breakdown of domestic-only circulation exists. As a result, the US score of 4.5 is based on observable domestic issuance proxies rather than global market share. PayPal USD, issued by Paxos, provides the clearest domestic benchmark, with around $3–3.5 billion in circulation in 2025—more than the combined visible circulation across the other four jurisdictions. The US scores lower on regulatory readiness, however, as rulemaking across six agencies remains incomplete, and lower on deposit protection, where the unresolved question of yield-bearing stablecoins leaves bank funding more exposed than in the other regimes.

The GENIUS Act, signed in July 2025, is now in a six-agency implementation phase ahead of a July 2026 rulemaking deadline. The key unresolved issue is a regulatory loophole: while issuers are prohibited from paying interest, exchanges and affiliated platforms can still offer yield-like rewards that closely resemble deposit returns. The American Bankers Association argues this undermines banks' deposit base, while the crypto industry maintains that such rewards are distinct from interest. Whether that gap is closed now depends on the broader Digital Asset Market Clarity Act, which passed the House in 2025, cleared the Senate Banking Committee by a 15–9 vote in May 2026, and was placed on the Senate calendar the following month.

The Act prohibits permitted payment stablecoin issuers from paying interest or yield simply for holding a stablecoin. The OCC's proposed rule reinforces this, explicitly addressing the prohibition on issuer-paid interest and yield. The restriction is clear—but it applies only to issuers. It does not, on its face, prevent third parties, including crypto exchanges, affiliates and distribution platforms, from offering yield-like rewards to users who hold or transact in a stablecoin. This is the "loophole" at the centre of the dispute between the banking industry and crypto firms. An exchange such as Coinbase can reward users for holding USDC even though Circle, the issuer, cannot pay interest directly. In practice, those rewards can closely resemble deposit interest, which is exactly what the banks object to.

That distinction is why the broader Digital Asset Market Clarity Act has been held up. The contested provision in CLARITY is an attempt to address the rewards question. It is likely moving towards a compromise banning passive yield while permitting activity-linked rewards. The crypto industry resisted, the banks said the compromise didn't go far enough, and this standoff is one reason CLARITY's Senate timing remains uncertain.

No floor vote has been scheduled yet. Despite a White House target of July, passage by then remains uncertain: the bill must still be reconciled with the Senate Agriculture Committee's version, win sixty votes in the Senate, settle a contested ethics provision on officials profiting from crypto, and find scarce floor time before the recess and midterm campaign – too many variables for an easy passage. A slip into a post-election session, or into 2027, is possible. The US thus presents a paradox having the clearest statutory framework of the group, attached to the least settled political process.

Hong Kong's framework is complete, but its market is deliberately throttled

Hong Kong leads on legislative clarity and regulator readiness. Its Stablecoins Ordinance is in force, its supervisory guidelines are detailed, and it has already licensed two issuers. It scores lower on market access, deliberately throttled at two approvals against thirty-six applicants; lower again on circulation, since its coins are only at launch with little volume; and among the lowest on openness to non-bank issuers, reflecting a bank-first allocation.

Hong Kong's contest is over access. The HKMA received thirty-six applications under the ordinance, in force since August 2025, and granted only two licences in April 2026 to HSBC and to Anchorpoint Financial, the venture led by Standard Chartered with HKT and Animoca. A first-round approval rate near 5 per cent is a deliberate bottleneck, not a market. Mainland platform groups and Web3 aspirants that built sandbox operations, including those tied to JD.com and Ant International, remain outside, with no timetable for a second round.

The tension runs two ways. Domestically, a bank-first allocation pre-selects who shapes Hong Kong's payment infrastructure, favouring incumbents with established governance over the technology-native firms that pioneered the use cases. Strategically, Hong Kong must reconcile its hub ambitions with Beijing's caution toward private digital money and capital mobility — a constraint local clarity cannot resolve.

The United Kingdom's regime is clear, but its commercial viability is contested

The United Kingdom scores highest on deposit-protection stance: its unremunerated-reserve requirement and £40 billion ($52.9 billion) issuance cap form the most bank-protective design of the group. It scores lowest on circulation and adoption, as no sterling systemic coin is yet live, and only moderately on access, given the unresolved transition between the Financial Conduct Authority (FCA) and the Bank of England (BoE).

The UK's battle is over viability. UK-issued regulated sterling stablecoin are about $1.5 million according to the FCA with all GBP-pegged coins globally between ~$6–12 million. The split design in supervision places non-systemic coins under the Financial Conduct Authority (FCA), while stablecoin payment systems or service providers recognised as systemic by UK Treasury move into the Bank of England’s (BoE’s) regime, with the Financial Conduct Authority (FCA) continuing to oversee conduct and consumer protection. After significant feedback to its November 2025 consultation, the BoE revised its proposals in June 2026, dropping individual and corporate stablecoin holding limits and replacing them with a £40 billion temporary issuance cap per systemic stablecoin and is intended as a temporary macroprudential constraint rather than a permanent market-wide limit. It also raised the permitted share of backing assets held in UK government debt from 60% to 70%. Even so, the £40 billion cap, a layered supervisory approach and restrictions such as non-interest-bearing central bank deposits continue to fuel concerns that a sterling systemic stablecoin may face challenges to commercial viability at scale. A second, institutional tension persists: the seam between an innovation-minded FCA and a stability-minded BoE, and the cliff-edge a coin faces transitioning between them as it scales. With the BoE consulting until September 2026 before it moves into finalisation of rules and implementation drafting, none of this is closed.

Singapore's rules are settled, but its strategic direction is not

Singapore is the high-standards all-rounder, scoring strongly on regulatory clarity and readiness. StraitsX's SGD stablecoin is already in active circulation, while Paxos issues a regulated USD stablecoin under the Monetary Authority of Singapore framework, although overall volumes remain modest relative to global USD-denominated liquidity. Singapore's domestically issued circulating stock remains modest at $60–80 million across StraitsX's pair of XUSD and XSGD, and remains well below $150 million even when affiliated USD stablecoins are included. Its score is constrained primarily because enabling legislation has yet to be enacted and no issuer has formally received the "MAS-regulated stablecoin" designation.

Singapore’s contest is the quietest but still evolving. MAS finalised, alongside Japan, one of the world’s earliest dedicated single currency stablecoin regulatory frameworks in 2023, establishing a clear regime for regulated stablecoin issuance while implementation and market development continue to evolve. The framework is implemented, like in Japan, under Singapore’s Payment Services Act, but it differs compared to Japan as Singapore regulates at the issuer level.

Within Singapore’s ecosystem, licensed stablecoin issuance is led by StraitsX and Paxos (via its Singapore entity), both operating under MAS’s single-currency stablecoin framework. However, while licensed participants and in-principal approvals exist, no stablecoin has yet been widely and formally designated in the market under a distinct ‘MAS-regulated stablecoin’ label.

The deeper tension here is strategic. MAS is steering banks toward tokenised deposits through Project BLOOM and wholesale-CBDC settlement while simultaneously licensing stablecoin issuers, leaving it intentionally open which instrument ultimately will find market adoption and economic scale.

Japan opens the stablecoins market, but licensed gatekeepers hold the keys

Japan scores strongly on legal clarity and regulatory readiness, with stablecoin rules in place since 2023 and a three-tier issuer framework covering banks, trust companies, and registered fund-transfer providers. However, access is restricted, circulation remains limited, and openness to non-bank issuers is low compared with issuer-led regimes such as Singapore’s. All JPY-denominated tokens combined account for less than $50 million, with JPYC the largest at ~$18m.

Japan's contest is over control of distribution. Unlike Singapore, which regulates at the issuer level, Japan has adopted an intermediary-permissioned model in which market access depends on approval and compliance obligations imposed on domestic institutions responsible for issuance, custody and distribution. The market is open, but only on tightly controlled terms. Foreign stablecoins are permitted, but only through licensed Japanese partners, including megabanks and brokerages, rather than directly through their issuers. Whether a stablecoin is JPY- or USD-denominated, it reaches the Japanese market only through channels controlled by incumbent financial institutions. The framework is deliberately designed to ensure that banks—not crypto-native issuers—remain the primary gateway to the digital economy.

Foreign stablecoins such as Circles’ USDC entered in 2023 and Ripples’ RLUSD in June 2026 through SBI-linked entities. Circle is planning to work with Nomura to enable instant settlement of foreign currency for Japanese companies as early as 2027, according to Nikkei. A domestic yen stack is also emerging across tiers, from JPYC for retail use to trust-bank and megabank-backed institutional settlement rails built on platforms such as Progmat.

These differences are unlikely to converge, leaving fragmentation as the outcome

Ownership, distribution, interest rules, issuance caps and licensing thresholds reflect different national tolerances for disintermediation and will likely stay distinct. For larger financial institutions and banks adopting stablecoins for cross-border settlement, fragmentation and interoperability may prove a nearer challenge than concerns over deposit disintermediation itself – at least in markets in Asia.

One signal cuts across all five, deliberately keeping tokenised deposits outside the stablecoin perimeter and preserved their existing treatment, an indication that regulators expect the banking system's main response to be ‘bank money on-chain’ rather than bank-issued coins.

Towards a contest over infrastructure, not yield

The yield debate is only the tactical layer. As Emmanuel Daniel argues in The Future of Finance, stablecoin yield is a near-term skirmish; the deeper contest is over access to regulated payment rails and who ultimately shapes how money moves in the digital economy. A licence is therefore not just permission to issue a coin, but entry into the infrastructure layer of the next economy and whether that privilege accrues to banks or crypto-native issuers determines who builds tomorrow’s rails.

For banks, the implication is therefore less about yield competition and more about securing a position in the underlying infrastructure — before customers settle tomorrow’s transactions on someone else’s rails.

At the same time, USD stablecoin dominance is sharpening concerns around monetary sovereignty, particularly in Europe and currency volatile emerging markets, where regulators fear offshore dollar tokenisation could be used as potential channels of currency substitution.

For industry participants, this creates a widening gap between fintech optimism around stablecoin payments and regulators’ focus on liquidity risk, governance and systemic transmission. Yet across jurisdictions, a common direction is emerging: stablecoins used as money will be held to bank-like standards. Regulatory clarity is becoming a key determinant of whether stablecoin circulation will hit the projected $1.9-2 trillion in an industry base case scenario by 2030.

Subscribe for regular insights.

.png)

.webp)